Enterprise Value vs Equity Value Explained

Enter any corporate finance interview, eavesdrop on any M&A negotiation, or read any equity research report and you will come across two numbers that are used virtually interchangeably by people who have years of experience and have been trained to distinguish between them: enterprise value and equity value. Learning the distinction between these two ideas is not an intellectual undertaking – it is at the core of the acquisitions, sales, financing, and comparison of businesses. However, to most practitioners entering or furthering their career in finance the line is as blurred as ever.

It is no wonder there is confusion. Both the figures are a representation of what a company is valued at and in an informal discussion they are frequently used interchangeably. Yet they have completely different answers to questions. Enterprise value makes you know how much it would cost to purchase the whole business including its operations, assets and liabilities. Value of equity informs you of what remains to the shareholders after all the other financial claims are paid off. When analysts discuss the difference between the enterprise value and the equity value, they are actually discussing the difference between the overall price of a business and the price of an ownership of a business. Making such a mistake, even through a conceptual error, results in acquiring things at the wrong price, making wrong valuations and structuring deals in a poor manner.

This article takes a step through either of the concepts, both in a clear and practical manner. It discusses the calculation of every figure, the purpose of the terminal value in valuation and its influence on the figures, overviews all the main methods of company valuation employed in professional practice, and uses real life examples of companies to explain the application of the theory. You are about to be hired in a finance job, you are going through your first valuation model, you are working to figure out what your organisation is contemplating as a deal, you will find this guide written to provide you with a clear, useful base.

The Core Distinction: What Each Metric Is Actually Measuring

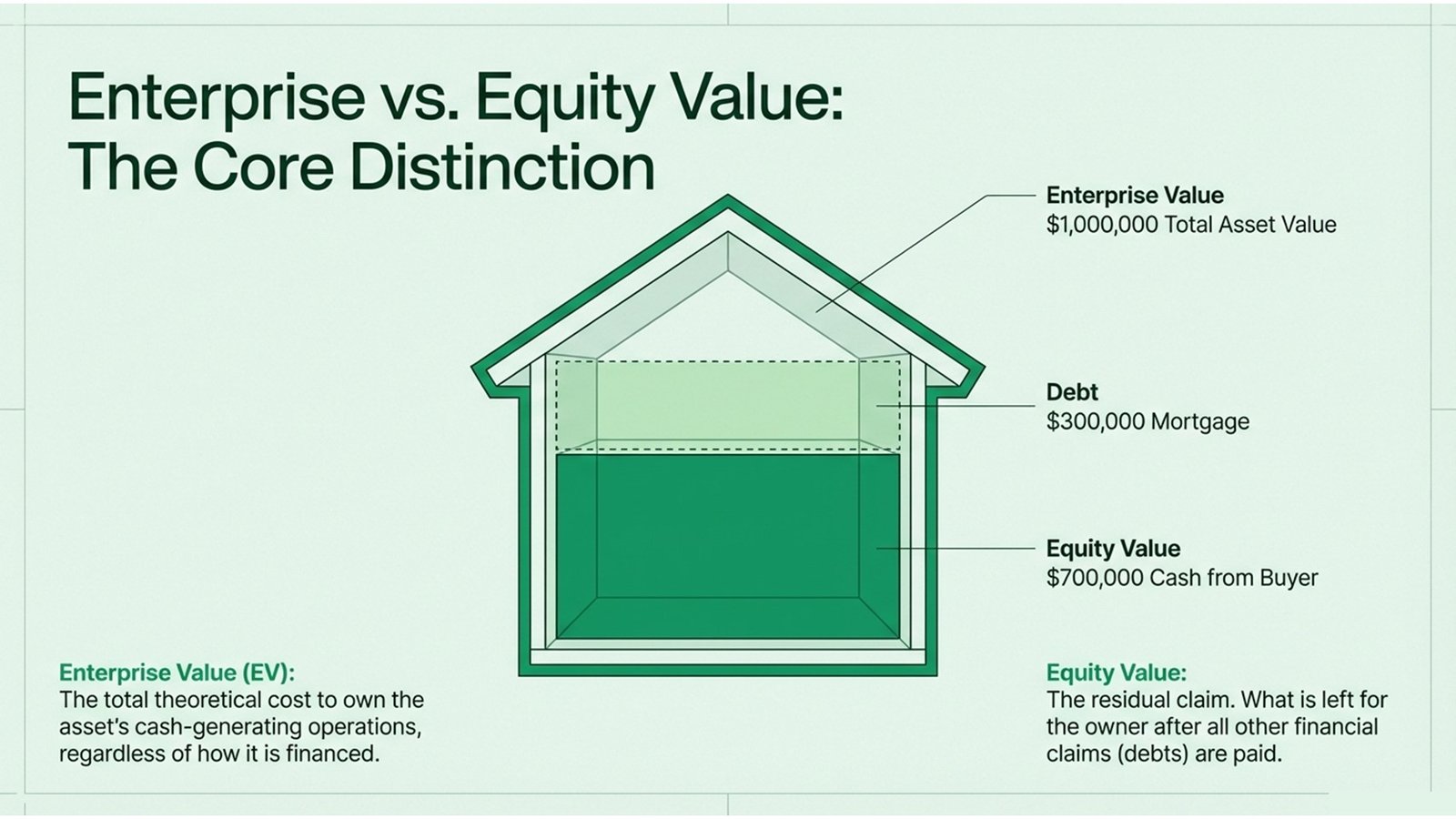

Enterprise value (EV) Theoretical total cost of acquiring a business – the amount you would pay to own all of its cash-generating business, whether it is financed or not. This is calculated by beginning with equity value (market capitalisation in the case of a listed company, or a negotiated purchase price in the case of a private company) and then increasing by net financial debt (total debt less cash) and then making adjustments to minorities, preferred equity and unfunded pension liability. The consequence is a capital-structure-neutral indicator of the operating value of a business – helpful because it enables you, exactly, to compare two businesses with very different amounts of debt equally.

The equity value, however, is the remaining claim, what is left of the ordinary shareholders after all debt holders and preferred investors have been paid off. In the case of a publicly listed company, it is just the product of the share price and shares outstanding (market capitalisation). In the case of a private company, this is calculated based on an agreed value of the enterprise, less net debt. The enterprise value equity value relationship is thus no contest, but an equation: equity value = enterprise value less net debt (inclusive excess cash). This bridge is among the most undertested notions in corporate finance since it compels one to ponder in detail about what is on the balance sheet of a business, and how it influences the claim of each party to the business.

A mere comparison aids in establishing the difference. Suppose you purchase a house worth a million dollars. Suppose the mortgage on the house is 300,000, the enterprise value of the house is 1 million – the total value of the asset. However, you, as the purchaser, just need to pay in the equity price: the seller (the seller has to pay off the mortgage or you have to pay it off) gets the cash: $700,000. And now imagine the seller had also retained in a cash account relating to the property the sum of 50,000,– the enterprise value would be reduced to 950,000,– since you are virtually getting back the cash. And this is exactly how the EV-to-equity-value bridge is applied to corporate transactions, and why advanced buyers will always consider net debt, not gross debt, when determining the cost of acquiring the company.

Table 1: Enterprise Value vs Equity Value — Key Differences

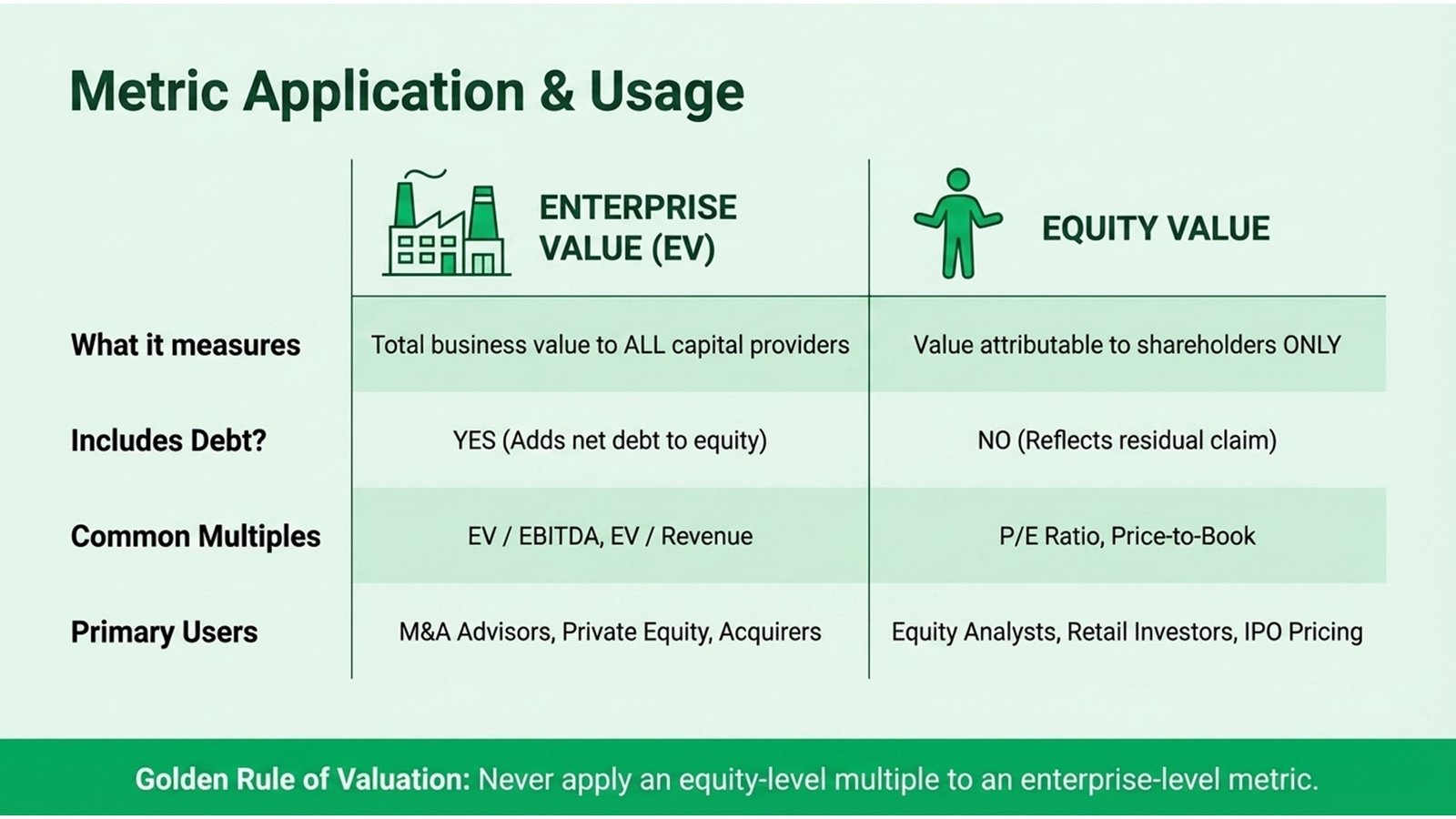

| Dimension | Enterprise Value (EV) | Equity Value |

| Definition | Aggregate value of the business to the ALL capital providers. | Value of shareholders alone. |

| Includes Debt? | Yes – adds net debt to value of equity. | No – reflects residual claim by equity holders. |

| Includes Cash? | Subtracts excess cash | All cash are included on the balance sheet. |

| Typical Use | M&A deal valuation, peer-based valuations. | IPO pricing, share based compensation. |

| Common Multiples | EV/EBITDA, EV/Revenue, EV/EBIT | P/E ratio, Price-to-Book, Price-to-Sales. |

| Who Uses It | Corporate finance, M & A advisors, private equity. | Investors in retail, equity research analysts. |

Five Key Principles for Applying These Concepts in Practice

The first step is to understand what enterprise value and equity value are all about. To effectively use them professionally, a discipline habit set that takes years to develop is necessary. What that experience appears to be is distilled into the following five principles.

Table 2: Five Key Principles — Enterprise Value and Equity Value in Practice

| # | Key Point | Why It Matters in Practice |

| 1 | Always Start with Enterprise Value | EV is the title figure in M&A and corporate finance. It is not the starting point of the equity value. |

| 2 | Net Debt Alters the narrative. | A firm that has a lot of cash and little debt will have a low EV than equity value. The reverse will be the case with a leveraged business. Always balance the sheet. |

| 3 | Multiples of EBITDAs are dependent on business types. | A software company with a 15x EBITDA and a manufacturer with a 6x are not mis-priced – the difference between the growth and capital intensity profile. |

| 4 | DFS Models are overtaken by Terminal Value. | The terminal value of a valuation in a typical 5 year DCF is usually 60-80% of total value. Insignificant changes in assumptions have significant valuation effects. |

| 5 | Combine Several Methods. | None of the methods of company valuation is absolute. The range of triangulation between DCF, comparable, and precedent transaction is credible. |

These five principles are not abstract, they manifest themselves in practical situations each week in the finance departments, strategy departments, and board rooms. The first mistake that junior analysts can make is picking the wrong metric to the situation: equity value when comparing to peers (providing spurious comparisons when leverage varies) or equity multiple to an EBITDA number (combining enterprise-level and equity-level measures). One of the most viable skills that a finance professional can develop is developing muscle memory related to what metric fits in what context.

Company Valuation Methods — A Working Survey

There exists no one right way of appreciating a business. Professional valuers rely on several methods of valuing the company at the same time and triangulate to a range of values instead of a specific figure. All the methods have their advantages and disadvantages and the art of valuation is to know what method to give most weight in a particular situation. Discounted cash flow (DCF) analysis, analysis of comparable companies (comps) and precedent transaction analysis are the three most popular.

DFS is the most rigorous conceptually of the company valuation techniques in that it is based on the actual cash that a business is likely to produce during its lifetime. The analyst takes the free cash flows and projects them over a forecast period of five or ten years, discounted at the weighted average cost of capital (WACC) and finally a terminal value in valuation is added in the valuation to reflect the value of the business outside the forecast period. The terminal value is typically determined through a perpetuity growth model (when the cash flows are expected to grow at a constant long-term growth rates indefinitely) or an exit multiple (Applying a market determined multiple to the last year of EBITDA or free cash flow). The following process flow describes the DCF methodology step-by-step.

The most popular market-based approach is the comparative company analysis (trading comps). It uses a target company as a comparison to the trading multiples of publicly listed counterparts – usually EV/EBITDA, EV/Revenue, or Price-to-Earnings. The reasoning is straightforward: assuming three comparable listed firms have an average price-to-EBITDA of 9x, and your target has a $50 million of EBITDA, then a valuation of $450 million would be a good starting point to estimate the enterprise value. Precedent transaction analysis resembles this, except that it uses the multiples paid in actual M&A acquisitions, which tend to exhibit a premium over trading comps – control premium and acquisition synergies. Collectively, these three techniques are the fundamental set of instruments of professional company valuation techniques employed throughout investment banks, private equity firms, corporate development groups.

Process Flow 1: Bridge from Enterprise Value to Equity Value

| Step | Action | Notes / Considerations |

| 1 | Calculate Enterprise Value | Begin with market capitalisation (shares x price) or use an EBITDA multiple of similar corporations. |

| 2 | Add Sum of Total Financial Debt. | Included are bank loans, bonds, and finance leases, and any off-balance-sheet obligations. |

| 3 | Lessen the Cash and Cash Equivalents. | Only use excess cash– do not include cash needed to operate to avoid over-deducting. |

| 4 | Accommodate Minority Interests. | Add back the value of the minority interest in case the company consolidates subsidiaries that it does not wholly own. |

| 5 | Adjust associates / investments. | Less the fair value of equity interest in other companies not consolidated on EBITDA. |

| 6 | Calculate Equity Value. | The outcome is the value which can be attributed to ordinary shareholders-divide by share outstanding to get implied share price. |

Process Flow 2: DCF Valuation — Step-by-Step

| Step | Action | Notes / Considerations |

| 1 | Project Free Cash Flows | Develop 5-10 years outlook of unlevered free cash flows – earnings before interest, after taxes, including the capex and working capital flows. |

| 2 | Determine the Discount Rate (WACC) | The cost of debt and equity is combined to form weighted average cost of capital and the proportion of the capital structure is used to weight them. |

| 3 | Discount Cash Flows Present Value. | Use the WACC on the cash flow each year that is projected to calculate future cash into current dollars (or other currency). |

| 4 | Calculate Terminal Value | Either use a Gordon Growth Model (perpetuity growth rate) or exit multiple of the cash flow in the last year. this is the end value in valuation – be careful. |

| 5 | Discount Terminal Value to Present | Take the terminal value and move the terminal value back to today at the same WACC. Record the magnitude of this value, compared to the total – this is the sensitivity point. |

| 6 | Add to Enterprise Value, and Cross to Equity. | Total PV of cash flows + PV of terminal value = Enterprise Value. Next proceed as in Process Flow 1 to obtain Equity Value. |

The Role of Terminal Value — and Why It Deserves Careful Scrutiny

Among all the elements of a discounted cash flow model, terminal value in valuation is the most valuable and the most abused. The terminal value in a typical five-year DCF model takes between 60-85% of the calculated enterprise value. This implies that a model that seems to be based on in-depth, year-by-year cash flow forecasts, is in fact dominated by one assumption regarding the ultimate value of the business after the explicit forecast horizon is over. This is not a weakness of the approach – it is an economic fact that the larger part of the value of a company is the long-run cash-generating capability. However, it does imply that the assumptions that underlie terminal value are as worthy of examination as the near-term estimates.

Both of these methods of estimating terminal value in valuation have significant weaknesses. The perpetual growth model is very sensitive to the assumed long term growth rate – even a difference of one percentage point in the growth assumption will alter the terminal value (and hence the enterprise value) by 20 to 30 percent in a leveraged business. The exit multiple method does not have this sensitivity, but introduces the existing market pricing in a model that is expected to be market sentiment free. Practically, most analysts will run both methods and see whether they give similar results – a big difference is an indicator of a need to re-examine the assumptions.

An established case of the terminal value sensitivity in action can be seen in the acquisition of LinkedIn by Microsoft in 2016. Microsoft paid about 26 billion, which is a 50 percent premium of the existing share price of LinkedIn. To support such a high premium in a DCF meant bold assumptions concerning the further growth of revenue and margin at LinkedIn over the long run, which were fueled by a high terminal value in valuation. Critics then claimed that the assumptions were optimistic; proponents that LinkedIn would continue to grow above-market in the decades to come noted that the network effects would support the growth. It is a prime example of why terminal value is the battleground in most deal valuations – it is where the bull case and the bear case come into most conflict and where the valuation team analytic skills are most on display.

Challenges, Common Errors, and Lessons from Real Transactions

Even practiced finance people commit errors in the use of enterprise value and equity value notions. The most frequent mistake is the mismatch of categories: it uses a multiple of an enterprise scale (like EV/EBITDA) but then compares it to an equity-level indicator, or the other way round. This is commonest when analysts operate using pre-modeled templates or extract data using financial databases without examining what is in the numerator and denominator. The resultant effect can be a valuation that is either 10 to 40 percent over or undervalued – a material error in any transaction setting.

A second issue is the non-operating items treatment in the bridge between the enterprise value and equity value. Other things like unfunded pension liabilities, earn out obligations, environmental remediation costs and operating lease commitments were not included in the calculation of net debt in the past. With more recent accounting standards, especially the implementation of IFRS 16, which has led to operating leases being reported on the balance sheet, these should be evaluated more carefully. Firms in the airline, retail and hospitality industries were some of the worst hit, as they are likely to have huge lease commitments. Professionals working with company valuation methods in these sectors must ensure their EV-to-equity bridge captures these liabilities correctly, or the implied equity value will be meaningfully overstated.

An example of EV and equity value framing in the context of deals is a lesson learned about the failed merger talks between Kraft Heinz and Unilever in 2017. Kraft Heinz has publicly offered to acquire Unilever in a deal worth the enterprise value of around 143 billion. The offer was promptly rejected by the board of Unilever and analysts remarked that the implicated EV/EBITDA multiple was low in comparison to similar deals in the consumer staples industry. The practitioner lesson is that it is always a deal framing exercise that the buyer anchors on the enterprise value (the total cost) and the shareholders of the target on the equity value per share (what they get). The difference in the conceptualisation of enterprise value as opposed to equity value by each side is also a common factor in why first bids are turned down, even when each side feels that a transaction is strategically sound.

Conclusion: Actionable Insights for Your Professional Practice

Enterprise value vs. equity value is not merely a technicality but a prism through which each deal, each acquisition and each financial model is viewed. Those practitioners that are conversant with both concepts, and who know how they relate to each other via the debt bridge, the choice of the valuation techniques, and the assumptions inherent in terminal value in valuation, are indeed more qualified to contribute to high-stakes financial debates, irrespective of their particular role.

To the more career-adaptable, the immediate best thing you can do is to create and stress-test your own simple DCF model. Begin with a company with which you are familiar – maybe in an industry in which you track – and develop a five-year cash flow projection. Of special interest is what occurs when you vary your terminal growth rate or exit multiple. The only better way to build any intuition about why terminal value in valuation should receive such special consideration is to watch the overall enterprise value change by hundreds of millions to respond to an insignificant change in the assumption.

In the case of senior, or strategically-minded people, the pragmatic need is to make sure that when your organisation is considering acquisitions, selling assets or raising capital, the team has always in mind what value measure they are talking about. Always demand a clear EV-to-equity bridges in any deal memo. Oblige all peer benchmarking to be done on enterprise-level multiples in comparing businesses with varying capital structure. And when considering DCF-based valuations, always question how much of the entire value is in the terminal value, and how the long-term growth assumption can be justified.

Lastly, it is important to remember that none of the key methods of company valuation methods is the truth. Both are models of reality, and both are constructed on the basis of assumptions which can and do disagree with reasonable professionals. Valuation is not aimed at coming up with a single, specific number but rather at creating a coherent range of numbers, based on market evidence and sensitivity tested. The professional who has the deepest insight into enterprise value versus equity value, who regards terminal value assumptions with the necessary scepticism, and who cross-checks across a variety of approaches with confidence is the one that garner trust in the room – be it a boardroom, a deal team or a job interview.