Economic Trends Impact Valuation 2026

In the year 2026, the global economy will be quite different as compared to the one that the analysts were sailing through only a few years back. After a long spurt of vigorous monetary tightening, interest rates are cooling into a new normal where they are higher than it was a decade before 2022. Supply chains are being redesigned due to geopolitical fragmentation. Artificial intelligence is also starting to change productivity curves in such a way that they remain hard to cost into long-term predictions. To anyone who does business valuation work, be it in corporate finance, in the private equity, investment banking or strategic planning, the perception of the economic trends to which the valuation of companies is subject has never been more pivotal.

The article is addressed to junior to mid-level professionals who are not only practising valuation actively but also towards a position that involves valuation. It is not focused on giving a theoretical overview of macroeconomics, but rather a practical argument of why macroeconomic literacy should be at the center of every analyst. An ideal DCF model that is constructed with assumptions that are based on not taking into account the current economic environment will always come up with results that are misguiding instead of informative.

The subsequent sections discuss five key economic forces that will transform valuation in 2026, go through the steps of the analysis to integrate the said forces in the models, the pitfalls practitioners may encounter, and the lessons that can be learnt based on actual examples. In all this, it is about developing the type of judgment that allows analysts to run models and not the types of analysts who are able to think.

Five Economic Forces Reshaping Valuation in 2026

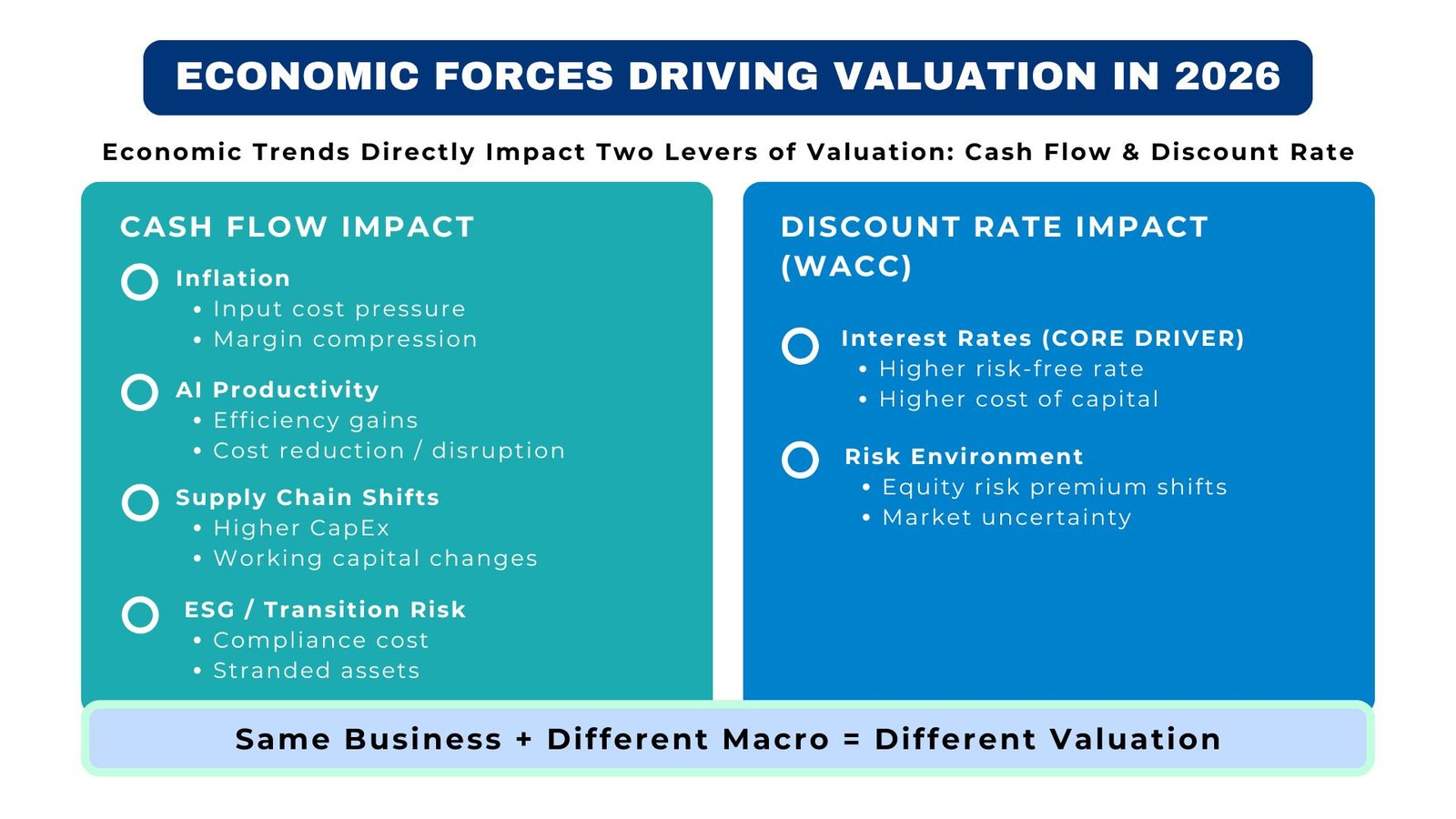

Valuation does not take place in the macroeconomic environment, but is an input. The five forces listed below have a direct impact on the cash flow that a business is likely to execute or the discount rate of the cash flows. The combination of them constitutes the most crucial group of economic variables in the valuation of companies that practitioners must comprehend and estimate in 2026.

| Economic Force | Primary Valuation Impact | Key Metric to Watch |

| Elevated interest rates | Increased WACC; shrunken equity multiples. | Policy rates of the central bank; 10-year yields on treasury. |

| Persistent inflation | Margin pressure; actual erosion of cash flow in reality. | Core CPI; the index of cost of inputs in sectors. |

| AI-driven productivity shifts | Industry upside or disruption risk of revenue. | Adoption of AI; capital investment in R&D. |

| Supply chain realignment | CapEx intensity; changes in working capital cycle. | Investment Reshoring data; logistics cost indices. |

| ESG and transition risk. | Stranded asset exposure; regulatory cost. | Carbon pricing; The score of ESG rating agency. |

Table 1: Five Economic Forces and Their Valuation Implication

The most immediate and machine direct force is the interest rates. Increase in discount rates decreases the present value of future cash flows all other things held constant. A business with a 7% WACC that results in 10 million of free cash flow every year may have a terminal growth rate of 2% and thus have an enterprise value of about 143 million. Restate that WACC to 9% – which is a credible change in a more-rate setting – and the identical stream of cash flow suggests an enterprise value of about $100 million, a decline of about 30, with no alteration in the underlying business performance. This is not an abstract idea, it is the experience of many portfolio companies and takeover targets revaluated between 2022 and 2025.

Although the inflation has slowed down in most of the developed markets, it still puts pressure on the margins of industries characterized by stickiness of input costs as well as low levels of pricing power. The emerging trends in business valuation that will be the most obvious in 2026 are an increased focus on analysis of inflation pass-through: to what extent can a business reliably transfer the inflation in the cost of inputs to the customers without losing its volume? Firms with strong brand equity or that have contractual mechanisms of pricing i.e. in infrastructure businesses with CPI-based revenue terms have a valuation premium as compared to firms that are at risk of spot pricing in competitive markets. The analysts that are able to measure this difference are bringing real analytical value.

The latest and most unpredictable of the five forces is the AI-driven productivity. There are some businesses which are literally realizing efficiency improvements – lower head count needs, decreased product development time, decreased customer acquisition costs, which enhance free cash flow margins in a manner that could not be seen two years ago. Others experience interference of the current revenue streams especially in services that are intensive in knowledge. The problem with the valuation analysts is that AI productivity benefits cannot be easily separated and more difficult to maintain under a competitive equilibrium in which competitors will ultimately match the same tools. The more defensible method of analysis is cautious, modest handling of AI positive effects, which is backed by evidence of particular operational performance as opposed to sectoral exuberation.

Integrating Macroeconomic Assumptions into the Valuation Process

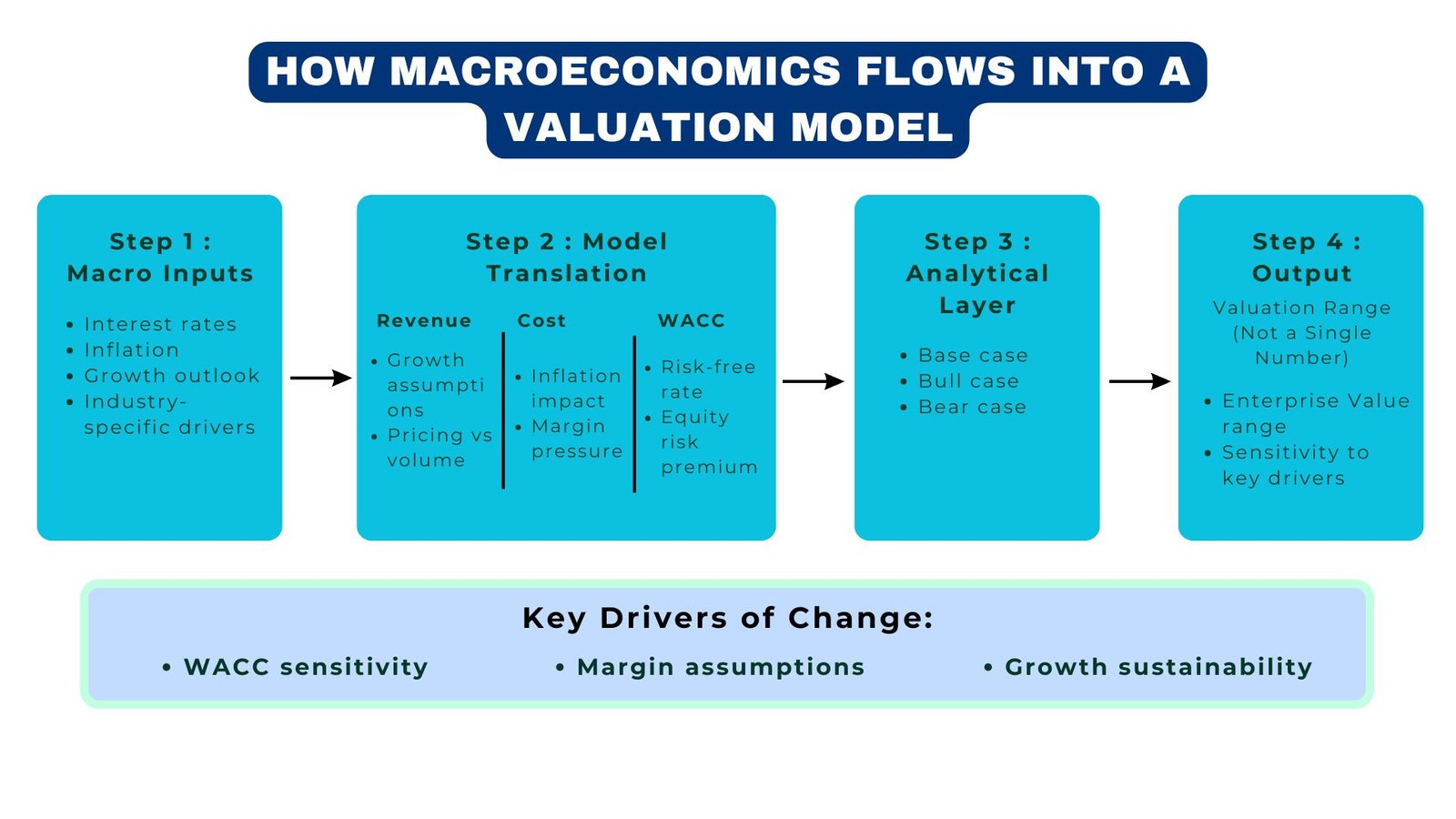

One thing is to realize that economic forces are relevant; another is to have an organized procedure of integrating them in a valuation model. Most junior analysts use macroeconomic assumptions as an input in itself, i.e. put in a consensus growth rate of GDP and leave. The more experienced practitioners go in a more layered fashion tracing the influence of macro conditions on each line of the model in a systematic manner. The following workflow represents the manner in which an investment bank or a private equity firm with a mid-market would tend to approach the economic trends with regard to valuation of the company in a live mandate.

| Process Stage | Activity | Output |

| Macro Environment Mapping | Determine the best 3-5 macro variables of this business and industry. | Macro sensitivity matrix |

| Historical Correlation Analysis | Experiment with the historical changes in the revenue and margins with respect to the macro variables. | Summary of regression/correlation. |

| Scenario Construction | Construct base, bull and bear macro with the use of clear assumptions. | P&L and cash flow 3-scenario model. |

| WACC Calibration | Modify cost of equity and debt to indicate prevailing rate environment and premium of risk. | Table of sensitivity of updated WACC. |

| Stress Testing | Bear-case macro scenario model; determine value at risk. | Lower range of enterprise value. |

| Comparables Reconciliation | Multiplied market trading and transaction information against cross-check. | Bridge chart Valuation football field or bridge chart. |

Table 2: Process Flow – Macroeconomic Assumptions into Valuation

Macro environment mapping stage is an area that should be given more consideration than it is given. All the macro variables do not equally expose all businesses. A food company that is domestic oriented takes the wage inflation, as well as consumer spending patterns seriously, yet it is comparatively immune to currency movements. An exporter of technology hardware, in its turn, has all three risks at the same time currency risk, tariff risk and disruption of the supply chain risk. The initial step of a diligent analyst is to determine which particular macro levers have the highest chance of shifting the needle on the company under consideration. and therefore, follow the levers on through the income statement and the balance sheet.

The imperfect historical correlation analysis offers an empirical basis of assumptions of forecasts. When the contracting trend of EBITDA margin of a firm is an average of 80 basis points on a percentage of increase in raw material cost indices in the last five years, the relationship should form the basis of margin assumptions in the model despite the management being more optimistic. Analytical credibility is achieved by demonstrating your work: by demonstrating that your assumptions are based on historical patterns that can be observed, and modified to reflect any change in the structure of the business.

Real-World Cases: How Economic Conditions Moved the Needle

Concrete structures are made practical by means of particular illustrations. The next two instances portray the economic factors in company valuation as to how they played in practice in the businesses that went through the post-pandemic macro environment and what analysts and acquirers learned about them.

The initial scenario is an example of a mid-sized German manufacturer of industrial components, on which an evaluation of a private equity buyout occurred in the end of 2023. When the business was first screened, it had a trailing EBITDA of 38 million Euros and free cash flow was growing steadily. The first DCF with an assumption of a 2021-vintage WACC of 6.5% implied that the enterprise value was around the figure of €520 million. As deal team revised the WACC to be consistent with the current rate environment, i.e. including a risk-free rate of 4.2% and an increased equity risk premium, the recalibrated discount rate shifted to 9.1%. The revaluated enterprise value when the assumptions relating to cash flows were otherwise the same reduced to a figure of 340 million Euros. The seller who is pegged on the valuation that were made during the low-rate period did not accept the first offer. The transaction was restructured with an earnout, finally closing at an amount that was close to 370 million Euros. The moral of the story: buyers and sellers in 2024 and 2025 will have important valuation gaps, but these will be caused by different implicit assumptions about the discount rate environment, rather than the disagreement regarding the business itself. Analysts that were in a position to explain this dynamic well, not only through model output, but in plain, easy-to-understand language, were priceless in filling those gaps.

The second is the case of a US-based retail chain that has hired an advisory firm to evaluate strategic choices, such as a prospective sale, at the beginning of 2025. The firm had low EBITDA margins of about 8 per cent that are common in the brick and mortar retailing. The inflation in wages had reduced the margins by 150 basis points in the past two years and the projection was based on a recovery that was half. When the analysts developed a stringent inflation pass-through analysis, which involved the ability to test how much of the wage cost growth could be compensated by pricing, they discovered that the business had a low pricing power owing to the presence of the e-commerce. This observation had a significant impact of decreasing the sustainable free cash flow forecast. The resultant DCF suggested that there was a significant difference between fundamental value and management anchor and this enhanced the sale process greatly. The larger point is indicative of an emerging trend in the valuation of businesses, which is that inflation is not a homogenous phenomenon. Its effect on valuation will be solely based on the price power and cost structure of a given business that is being reviewed.

Challenges Analysts Face and How to Navigate Them

Including macroeconomic thought in the process of valuation is challenging in thought and operationally difficult. The challenges that analysts regularly face at all ranks are recurring and can, upon being not dealt with properly, compromise the integrity of the final product. Being aware of these challenges and possessing feasible solutions to deal with these challenges is among the development of authentic professional competence.

| Challenge | Root Cause | Practical Solution |

| The anchoring effect on outdated multiples. | Re-rating in the market that has not been captured in the choice of comps. | Compensate to trailing 12 months; articulate re-rating. |

| Macro assumptions inconsistency | Inflation took as revenue and not cost structure. | construct a macro assumptions page; connect all drivers. |

| Delusion in point estimates. | Projections given out of range of scenarios. | There must always be a base, a bull and a bear; measure important sensitivities. |

| WACC calibration errors | Stale data from which beta and risk premium were obtained. | Recalculate beta using existing 2 year window; current estimates of ERP. |

| Living in ignorance of qualitative macro signals. | Designed without reading the central bank instructions or outlook of the policy. | Add a macro briefing page with referencing to critical forward indicators. |

Table 3: Macro – Integrated Valuation Analyst Challenges

The tendency to base the current value on old multiples is perhaps the most common error in the present day practice. The valuation multiples that were experienced in 2019 to 2021 when the rates were close to zero and liquidity is high cannot be used as an accurate reference point to most asset classes in 2026. In the 2022 to 2024 re-rating, infrastructure assets, technology companies and consumer businesses were all re-rated dramatically. An analyst who constructs a similar company analysis with the transactions of 2020 or 2021 without correcting this re-rating will systematically overprice the target as compared to what the current market will actually pay. The remedy involves data sanitization (with recent comparables) and narrative transparency (as to why the re-rating is needed to a client who, perhaps, is stuck on older reference points).

The discrepancy in revenue side macro assumption and the cost side macro assumption is less obvious but is just as fatal. The most frequent mistake is to assume 5% annual growth in revenues, part of which is caused by inflation price increase, and keeping operating cost margins constant, that is, implicitly taking it that wages, energy, and input costs are not increasing at the same rate. In a situation in which the two sides of the income statement are drifting in opposite directions because of inflation then this inconsistency causes an unrealistically rosy trend in the margin and overstates free cash flow. The surest structural re-fix is to construct a unified macro assumptions page a single reference tab in the model which connects all the other line items in the model with an inflation, interest rate and growth assumption.

Lessons Learned and Emerging Best Practices for 2026

The last three years constituted an actual stress test to valuation professionals. The acceleration in the rate differentiation, the continuing inflation and the advent of AI as a variable of productivity have all made a reassessment of assumptions that the profession had regarded as established. The habits and disciplines that were applied by the analysts and firms that came out of this period unharmed are worth recording as lessons.

| Stage | Best Practice | Reasons Why It Will Matter in 2026. |

| Model Setup | Building a specific macro assumptions dashboard. | Makes sure that all drivers are auditable. |

| Forecast Construction | Differentiate between pricing and volume based growth in revenues. | Headline growth is misleading but real volume speaks otherwise. |

| WACC Estimation | Take existing risk-free rates; re compute beta after every 3 months. | Systematic mispricing in volatile rates is caused by stale inputs. |

| Scenario Analysis | Add a case of macro shock (e.g. recession or rate spike) | Offers downsizing insurance to clients and deal teams. |

| Communication | Make plain-English explanations of the macro assumptions on the executive summary. | Decision-makers do not necessarily know the models: transparency fosters credibility. |

Table 4: Process Flow-Most Optimal in 2026 in Macro-Integrated Valuation

Among the most obvious lessons of the valuation dislocation of 2022 to 2024 is that the economic trends on the company valuation cannot be considered as noise. They are structural inputs which cannot be vaguely recognized at all. Companies that had a disciplined procedure of calibration of WACCs maintained their risk-free rate and equity risk premium estimates current at least quarterly generated valuations that stood much better on the test than those calculated using annual or ad-hoc updates. At best, this field can no longer be regarded as a distinguishing ability in most credible advisory and investment companies; it is now regarded as a minimum requirement.

The second and no less significant lesson is the one that deals with communication. The technically most rigorous model in the world is not of use when the analyst is not able to explain to a CFO, a board member, or a client, who does not read spreadsheets, the main assumptions underlying the model. The risk of communication discontinuity between the decision-maker and analyst increases as the new emerging trends in business valuation are increasingly complex in the macro sense. The most effective practitioners fill this gap by starting with the story which is what is the macro story, what does it mean to this business, and what are the implications of the valuation and then going on to show the numbers. The story should not be substituted with the figures but approved.

Lastly intellectual humility is not a mushy ability, it is an analysis faculty. Those analysts who performed most in the recent macro volatility were those who persistently constructed and reported ranges, as opposed to point estimates, who revised their assumptions as new data came in as opposed to defending models that were stale and were open with clients about the restrictions of any forecast constructed on a fast changing macro basis. This posture gains credibility with time and it is becoming the norm that is required by the advanced clients and employers.

Conclusion: Actionable Insights for Practitioners

The point of intersection between macroeconomics and valuation has never been ignored. The difference is the extent to which it will be important in 2026, the rate at which the variables under consideration are changing and the complexity of the parties that are going to audit your work. Economic factors in company valuation, including the interest rates and inflation, as well as the disruption of the supply chain or AI productivity, are no longer the background factors. They are foreground variables which should be in the middle of all the valuation structures.

In the steps that practitioners can take now to apply these insights, a few can be taken into consideration. First of all, audit your current models of valuation: do the inputs of WACCs reflect the current situation, are the macro assumptions internally consistent and has there been a recorded scenario analysis? Otherwise they are priority fixes. Second, establish your own macro monitoring routine: which are the four or five economic indicators that best reflect the industries you are reporting on and look at them at the end of every month. Decisions of interest by central banks regarding rates, inflation reports, indices by purchasing managers and indices of specific sectors on the costs are all available publicly and are directly related to assumptions on forecasting.

Third, exercise expressing macro-to-valuation linksages in a normal language. Select one of your assumptions of your next model, e.g., the rate of revenue growth, and compose two or three sentences about the precise economic conditions of the macroeconomy that you believe validate that assumption and what would have to happen to prove that assumption incorrect. It is a drilling workout that makes you think analytically and ready to take the type of inquiries that the senior colleagues and clients will pose. The purpose behind the incorporation of economic trends on company valuation is not to complicate the models, rather, it is to make it more candid, more justifiable, and generally more beneficial to those who make decisions based on the models.

The emerging trends in business valuation that are manifested in 2026 more complicated macro environments, more focus on scenario analysis, increased demands on analytical transparency is a real improvement of the professional standards. Complexity embracing analysts who develop habits of working through it in a systematic way and who learn the communication techniques to make it understandable will be perfectly placed to not only perform good work, but to be entrusted to do so. It is that trust, which comes with rigour and clarity, that will stand the test of time as far as the economic conditions will constantly be in a state of flux in a profession.