Step-by-Step DCF Valuation Guide

The center of the finance is valuation. The capacity to come up with a defensible opinion of the value of a business will make the difference between a legitimate and a speculative analyst, whether it is a merger, an investment target, or an equity research report. Of all the tools that a financial analyst possesses, the discounted cash flow company valuation is the most intellectually exercising and highly regarded. It makes you consider deeply the economics of a business behind it, its growth path, its profitability, and its capital needs and the risk inherent in all those forecasts.

However, it might be a daunting task to be a junior or mid-level professional and go through with DCF analysis. The calculations include multi-year projections, assumptions of terminal values, and calculations of the weighted average cost of capital all of which have their own complexities attached. This guide is aimed at trying to unravel that complication. Instead of addressing DCF as black box, It takes a systematic, practical approach, using real-life examples and real-life analytical challenges which practitioners face on a day-to-day basis.

This is a guide that can be used by analysts who are in the profession or are in need of improving their technical advantage. At the end, you are expected to be capable of building and defending a DCF model in a business context, where the most important sources of value reside, and be able to effectively communicate your result to your stakeholders. The model can be used in any industry, manufacturing, technology, and consumer goods, as the rationality of future cash flows is common to all.

Learning Building Blocks of a DCF.

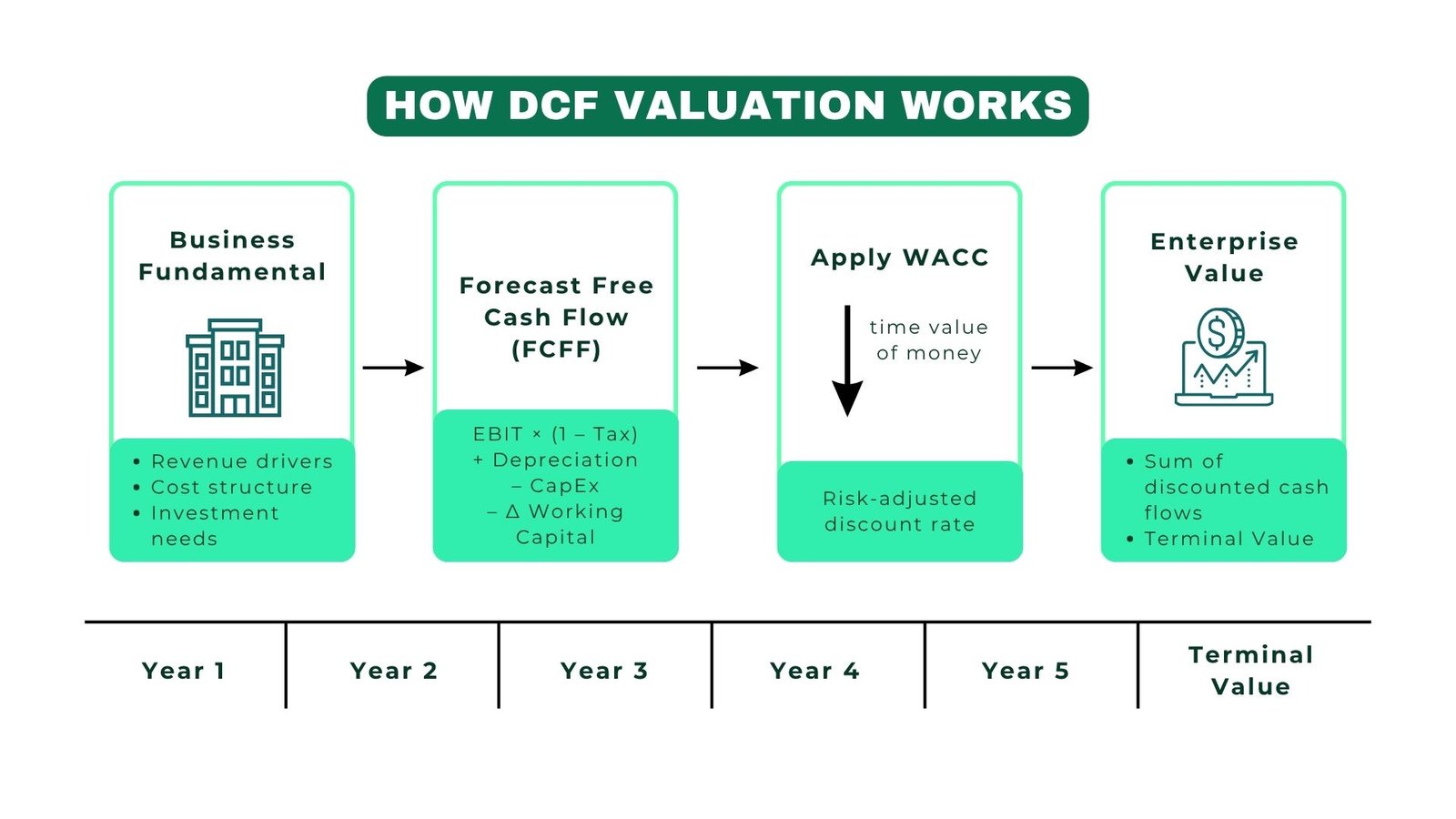

At some point before developing any model, it is best to have an idea of what a DCF is actually doing. The main assumption is easy, a dollar today is better than a dollar tomorrow, due to time, inflation, and risk. The way that this insight is operationalized in the discounted cash flow company valuation is to project the free cash flows that a business will produce over a forecast horizon – usually 5-10 years – and discount them back to the present value with a rate that reflects the riskiness of those cash flows. This has the effect of creating an internal value to the business based on its core, and not market feeling.

The forecast cash flows and the discount rate are the two major inputs. The free cash flow to the firm (FCFF) is the amount that the company has left to cover the operating expenses and capital investment requirements yet remains to cover debt obligations. This is computed by taking the product of EBIT and (1 less tax rate), then it is multiplied by the depreciation, amortization, working capital change and capital expenditure. To get this number correct, it would be essential to have a deep knowledge of how the business works not only by reviewing an income statement but also by knowing what promotes the growth of the business, what the cost structure is, and how aggressive the business would have to be to maintain growth.

The most frequent discount rate in the corporate valuation is the Weighted Average Cost of Capital (WACC). It is a sum of cost of equity estimated based on the Capital Asset Pricing Model (CAPM) and after-tax cost of debt weighted by the capital structure of the firm. Increased WACC implies increased perceived risk and since it appears in the denominator of all discounted cash flow calculations, even a small change in WACC can have a disproportionate impact on the ultimate valuation. This is one of the most significant issues that a junior analyst should internalize at the beginning.

The Five Key Steps in Building a DCF Model

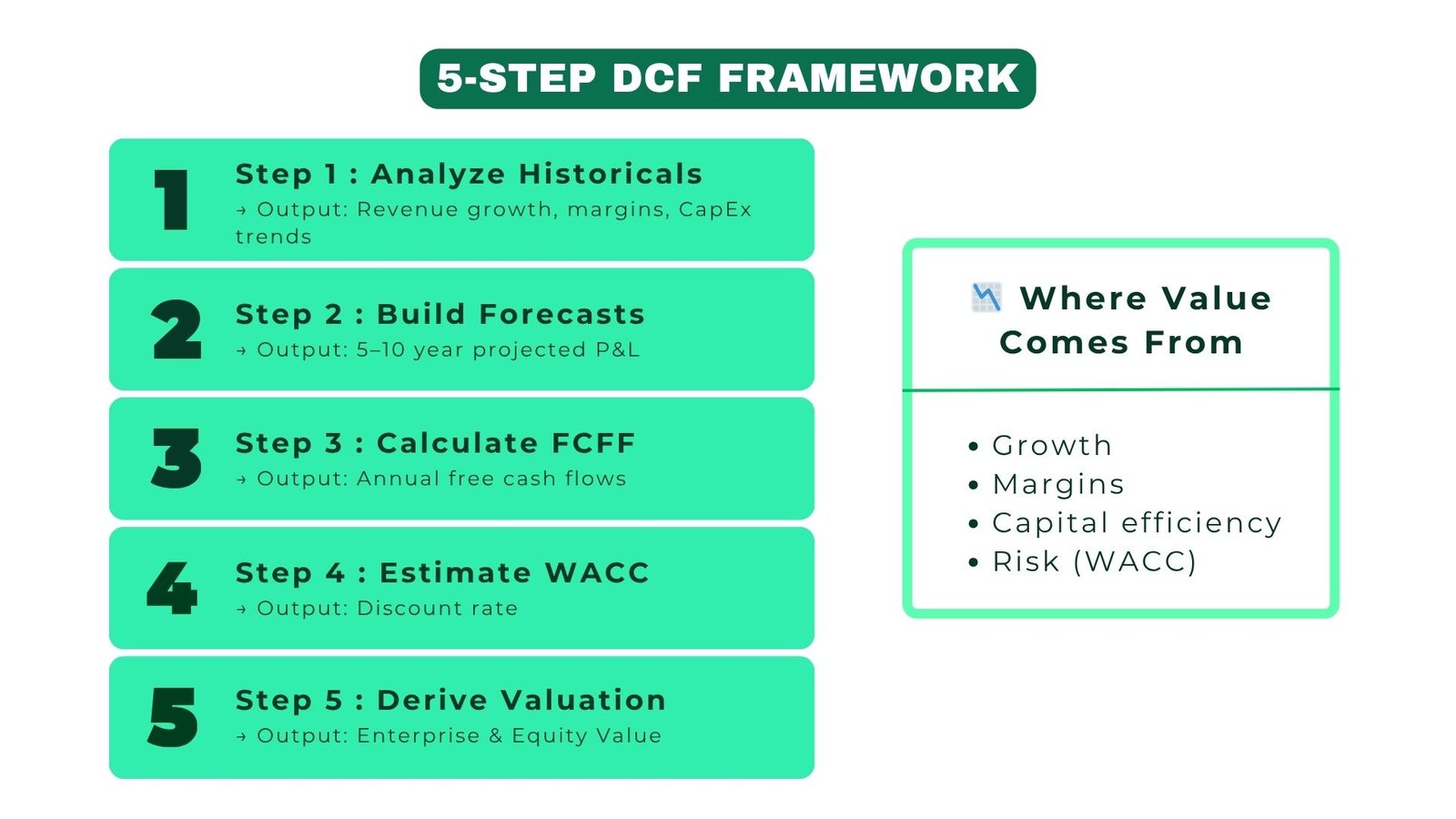

Moving in a methodical way to DCF minimizes the chances of error and makes the defense of every element of the model viable. Below are the five essential steps that professional analysts follow when conducting DCF modeling techniques for financial analysts in a real engagement context.

| Step | Action | Key Output |

| 1 | Review historical financials (3-5 years) | The CAGR of revenue, EBITDA margins, CapEx trends. |

| 2 | Develop revenue and margin projections. | Future 5-10 years P&L projections. |

| 3 | Derive free cash flow (FCFF) | The forecast period annual FCFF |

| 4 | WACC (discount rate) estimate | Single WACC value range of sensitivity. |

| 5 | Calculate terminal value and sum PV | Enterprise Value and Equity Value. |

Table 1: The Five Core Steps of a DCF Model

The first step, which is the analysis of historical data, is usually underestimated by junior analysts who are too keen to get into projection. But the past trends put a stake in the predictions. Assuming that a company has increased revenues at 8 per annum over a five year period, a projection of 20 percent growth would have to have a clear, specific thesis behind why the future will be radically different. You do not foresee but hope without that thesis.

The third step which makes or breaks the models is step three which derives free cash flow. Changes in the working capital are often poorly handled. A growing business will usually use cash in receivables and inventory to grow and this decreases free cash flow although reported earnings are increasing. Absence of this dynamic results in the systematic over optimism of valuation. Established analysts construct a separate working capital schedule and relate the changes to the assumptions of revenue growth.

Step five calculation of terminal value is especially worth considering since in a typical DCF, it comprises 60 to 80 percent of the total enterprise value. The two most used methods include Gordon Growth Model (that capitalizes the terminal year cash flow at the difference between WACC and a perpetual growth rate) or the exit multiple method (that utilizes an EV/EBITDA multiple applied to terminal year EBITDA). The combination of both approaches is a best practice and offers credibility to the final product.

Building and Stress-Testing the Forecast

The value of a DCF model lies in the forecast that it is based on. The majority of practitioners refer to modelling as 80% art and 20% science, that is, the mechanics are learnable, but to create a realistic projection one has to make a judgment, industry know-how, and an actual understanding of the competitive dynamics involved. This is because the procedure of creating a solid forecast is a logical process, which must be recorded and be articulable at each phase.

| Phase | Activity | Tools / Sources |

| Industry Analysis | Determine revenue drivers and benchmarking in the sector. | Peer filings, Industry reports. |

| Management Guidance Review | Audit prospective commentary in reporting. | Earnings calls, annual reports. |

| Revenue Build | Segment-by-segment or top line growth forecast. | Regression analysis, Excel model. |

| Cost Structure Modelling | Plot COGS and OpEx versus revenue. | Historical margin trends |

| CapEx & Working Capital | Connection to rates of revenue growth and intensity of assets. | PP&E plan, NWC analysis. |

| Free Cash Flow Derivation | Take all the above into FCFF calculation. | Model output validation |

Table 2: Process Flow – Developing the Operating Forecast.

Stress-testing should be done after the base case has been constructed. The standard starting point is sensitivity analysis, i.e. different WACC and the terminal growth rate at the same time. However, good analysts go an extra mile, and run a scenario analysis, which takes into account various macroeconomic scenarios: a bull case where the company is taking market shares forcefully, a bear case where margins squeeze under the pressure of competition, and a base case pegged to management advice and industry standards. The difference between mature modelling and mechanical number-crunching is the presentation of the range of the results, and not to give a single point estimate.

A practical case that can be discussed is the market research that a moderate size of a privately owned equity company carried out on one of the European automotive parts suppliers before a possible acquisition. The base case depicted a base value of the enterprise at around the value of about 420 million. However, when analysts tested the model on the basis of a scenario in which electrification of vehicles was taking place more quickly than projected, thus squeezing the demand of some legacy parts, the bear case valuation fell to the level of €290 million. The dispersion caused the acquirer to bargain a reduced entry value through an earn out mechanism which eventually cushioned the downside risk. It is applied practical DCF company valuation methods: not only to get a figure, but to get a deal put together in an intelligent manner.

Common Challenges and How to Overcome Them

DFC work has its pitfalls even when it comes to experienced analysts. Being familiar with such obstacles beforehand, and having how to go around them, is what makes one a reliable person in a work environment. The main problems are most likely to be clustered around three themes which are, circular references in the model, terminal value sensitivity, and treatment of non-operating items.

| Challenge | Why It Occurs | Recommended Fix |

| Circular references (WACC) | Enterprise value is relied on in debt and equity values. | Iterative or fixed capital structure. |

| Terminal value dominates | The present value is inflated by high growth perpetuity. | Growth of cap terminal at GDP; exit multiple check. |

| CapEx misclassification | Maintenance vs. growth CapEx was mixed up. | Single schedules that have asset intensity analysis. |

| Non-operating items ignored | Leases excluded in bridge, pension liabilities. | Equity value to EV Bridge, beware. |

| Overly precise forecasts | It is displayed with a growth of 7.3% suggesting false accuracy. | Round to significant intervals; give assumptions. |

Table 3: DCF Pitfalls and Pitfalls Solutions.

Circular reference issue is an exceptionally popular vexation of analysts who develop their initial complete DCF modeling techniques for financial analysts. WACC is also based on market value of equity and debt but this is based on what intrinsic value you are calculating. This is normally solved practically by assuming a given target capital structure – say 60 percent equity and 40 percent debt at market values – and maintaining this at all times during the model. This is the standard adopted in majority of investment banking environments.

Terminal value sensitivity is also to be mentioned. Take the case of a firm whereby the base case terminal growth rate is 2.5% that generates an equity value of $5.2 billion. A 50-basis points change in equity value to 2.0 percent would result in a 7.7 percent decrease in equity value to 4.8 billion dollars. A further increase to 3.0 percent makes the equity value to be 5.7 billion. This arithmetic explains why the assumption of terminal growth rate is never a waste figure; it should be based on long-run expectations of nominal growth of GDP of the concerned economy, which ranges between 1.5 percent and 3.0 percent in case of developed markets.

Linking DCF to Real-World Decision Making

A DCF model constructed in isolation, out of context, comparables, and with no clear decision framework, is not of much practical use. The discounted cash flow company valuation is always placed in a broader analytical context by the professional analysts. This generally implies the triangulation of the DCF output with trading comparables (peer group EV/EBITDA analysis), and transaction comparables (recent transactions in the industry). When the three methodologies are all in agreement i.e. DCF, trading comps and transaction comps, all are giving a similar range, then you have a defensible valuation. When they go in vastly different directions the difference itself becomes something to learn: is the market underpricing the company, or do you have over-optimistic DCF assumptions?

| Stage | Decision Point | DCF Role |

| Initial Screening | Should target be pursued any further? | Rudimentary DCF using industry standards. |

| Due Diligence | How can the value range be calculated in various circumstances? | Complete model and scenario and sensitivity analysis. |

| Pricing Negotiation | At what price will there be sufficient returns? | IRR and returns analysis overlaid on DCF. |

| Post-Deal Monitoring | Is the firm doing what it is planning to do? | Real and estimated cash flow monitoring. |

| Exit Planning | Which is cheaper between the business today and entry? | Current Assumptions DCF. |

Table 4: Process Flow DCF in the Transaction Lifecycle.

An effective case study in this respect would be the practice followed by a consumer goods company in North America that is considering the acquisition of a local brand in drink. DF intelligence with the base case assumptions provided an enterprise value of USD 180 million, which implies an EV/EBITDA multiple of 9.2x. The trading of comps with comparable businesses of beverages was trading at 10x-12x EBITDA which implied that the DCF was low. Recent deal transaction comps in the segment were at 11.5x on average. With such triangulation, the M&A team of the buyer knew that they could afford to bid higher without overpaying and the deal was closed at USD 195 million, which was still lower than the comps midpoint, and an inbuilt upside buffer.

This form of triangulation is the feature of the more practical DCF company valuation methods employed by analysts that realize that no one methodology can be complete. The DCF provides you with a basic anchor, the comparables with what the market will pay. The most effective analysts apply them both interchangeably to polish their thesis.

Lessons Learned and Professional Best Practices

After observing the failures of models on practice, skilled practitioners are likely to arrive at a number of habits that distinguish between high-quality analytical work and work that only happens to be technically correct. The first and the most significant habit is intellectual honesty on uncertainty. DF model forecasts the future – and future is unpredictable. Even the finest analysts admit that this is true and construct broad ranges of scenarios and explain the most important assumptions underpinning value instead of burying them on the footnotes.

Formal hygiene is also of great importance. A structured model must be auditable: all of the hardcoded assumptions must be labeled and not difficult to modify, all of the mathematical formulas must make sense and flow logically between the inputs and the outputs and there must be no black box between the line items. Within a workplace setting, your model will be checked by other professionals, customers and occasionally the conflicting groups in a deal. The model that is difficult to follow is a liability, no matter how advanced the analysis is.

Lastly, it is the art of returning back to the business story that makes good analysts great. The figures of a DCF model are what you think about the competitive forces of a business, the quality of their management, the sustainability of their margins, and the tail winds or head winds they have in their industry. When an output of a model seems to be surprising, either too big or too small, the natural question is why, and it goes back to the particular assumption to produce that output. This is where it can be said that DCF modeling techniques for financial analysts are really analytical and not mechanical.

Conclusion: Turning Analysis into Action

Learning to do discounted cash flow company valuation is a life long task. It can be learned in weeks; the judgment is a years-long process. However, with junior and mid-level professionals, it is not about perfection but rather creating a system of approach that is defensible and can be executed in a consistent way and conveyed in a clear manner. This guide has covered the main building blocks: the core of what a DCF is doing, constructing a powerful forecast, based on historical analysis, stress-tested assumptions with the aid of scenario and sensitivity analysis, avoiding the common modelling pitfalls, and placing the output in the context of a more general valuation.

A number of practical steps that can be put to practice now to sharpen your skills are available. Prepare a DCF using published financial statements of a company that you are familiar with – a retailer, a manufacturer, a technology company. Make yourself explain why you are making each of the assumptions and then examine the resulting implied valuation against the present market price of the company. The difference – and your capability of defining it – is where the actual education lies. In practical DCF company valuation methods, it does not only depend on the accuracy of numbers but equally on the quality of your reasoning in an interview or on the job.

Be honest with uncertainty with the use of sensitivity tables. Construct at least two scenarios: a bear case and a bull case and be in a position to justify the most important factor behind the spread between them. Compare your DCF with at least one group of market analogs and, in case the two are very divergent, build an articulated thesis as to why. Training: Get used to being able to explain the key drivers of your model in three minutes to a senior colleague, otherwise you are not in a position to present your findings in a concise way. When done correctly, DCF analysis is not a spreadsheet project but a systematic approach to thinking of the future of a business and that is something to take seriously.