PSAK 48 Impairment Testing Guide

In the case of Indonesian companies that have expanded by acquisition, expanded into new areas, or have accumulated other intangible assets in their balance sheets, the learning to mastering impairment testing Indonesia PSAK 48 is one of the most impactful financial reporting practices. The impairment test makes a decision on whether the carrying amounts of assets ( especially the goodwill and the other intangibles acquired in a business combination) still represent an economic reality, or a loss has to be recorded in the income statement. This is not just a matter of compliance but a direct measure or indicator of reported earnings, equity and the believability of financial statements to the auditors, investors and the OJK.

The IAS 36 counterpart, PSAK 48 (Impairment of Assets) regulates when and how impairment should be measured, how recoverable amounts should be estimated, how impairment losses should be recognised and what losses should be disclosed. To finance practitioners in the Indonesian listed companies, M&A advisory practices, and audit practitioners, PSAK 48 is a recurrent, technically challenging task that increases in complexity with the volume and variety of the asset base of the entity.

The guide is a full-fledged old-fashioned handbook on how to be able to master impairment testing Indonesia: the principles of it, its application within industry, the analytical advantages, the example of how to apply the practice to cases, best practices of how to govern and document it, the common pitfalls between being able to perform a competent impairment testing and being able to perform financial reporting magnificently.

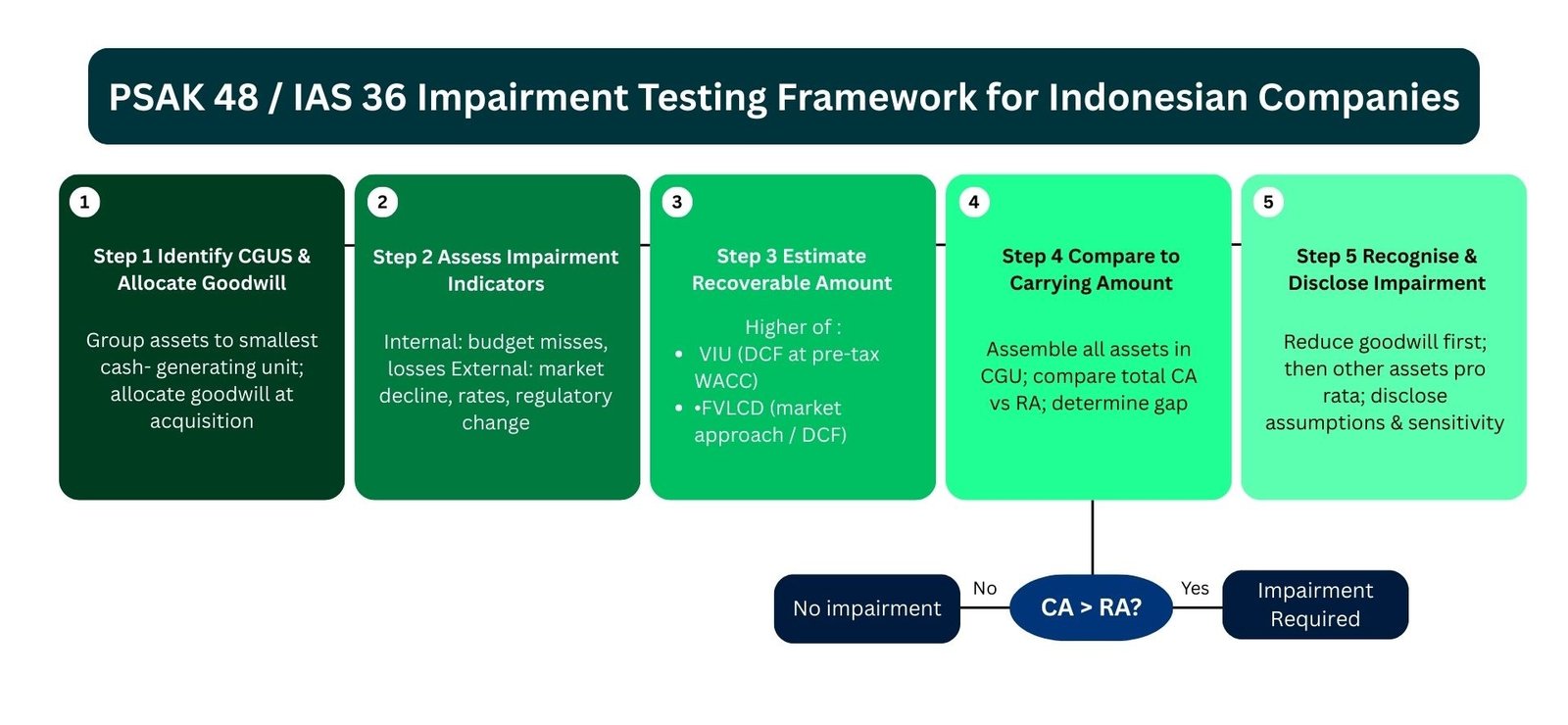

Figure 1: PSAK 48 / IAS 36 five-step impairment testing process for Indonesian companies

Key Concepts: Understanding Impairment Testing Indonesia under PSAK 48

Fundamentally, impairment testing Indonesia under PSAK 48 provides an answer to one question: is the carrying amount of an asset or a group of assets more than the amount that the business can possibly recover quality of it? In the event of the answer yes, the impairment loss so recognised should be immediately reflected in the income statement as a difference.

Recoverable Amount: Central Calculation

Recoverable amount consists of higher of fair value of an asset less disposal costs (FVLCD); and, value in use (VIU). PSAK 48 permits that recoverable amount should always be calculated as the higher of the two measures- making sure that such an asset is not written to be less than the more that the entity can recoup by selling it or by its continued use.

Value-in-use The present value of the future cash flows which are projected to be received on the asset or cash-generating unit, discounted at a pre-tax rate which represents current market judgments in the time value of money, and risk associated with the asset. Fair value less expenditures of disposal is the sum that may be raised by selling the asset at an arm-length transaction between knowledgeable, willing parties less the extra expenditures that may be directly related to the disposal.

Cash-Generating Units: The Unit of Account

Most assets do not produce autonomous cash flows, the value of the asset is realised by cooperating with other assets in the business. PSAK 48 covers this by stipulating that the impairment testing should be done at the level of the cash-generating unit (CGU): the smallest identifiable group of assets and the cash inflows of which are not significantly dependent on the cash inflows of other assets or other groups. The most significant structural decision in any impairment testing Indonesia engagement is correct CGU identification.

In its specific form, goodwill cannot be tested as such. It should be placed at the purchase date in the CGU or group of CGUs likely to achieve the synergies of the combination. This distribution forms a recurring, ongoing impairment testing requirement at the CGU level that continues until the goodwill has been removed out of the balance sheet.

Testing Requirement of Goodwill Annually

Contrary to other non-current assets, which are only tested in case there are signs of impairment, goodwill should be tested on an annual basis without exception, irrespective of whether an indicator of impairment has been identified. This renders the learning of impairment testing Indonesia to be a recurrence, calendar type of requirement to any Indonesian company that has ever made an acquisition and had recognised goodwill. Annual test should be done at the same time every year and methodology and assumptions employed in the test should be the same in one period to the other unless change is justified and disclosed.

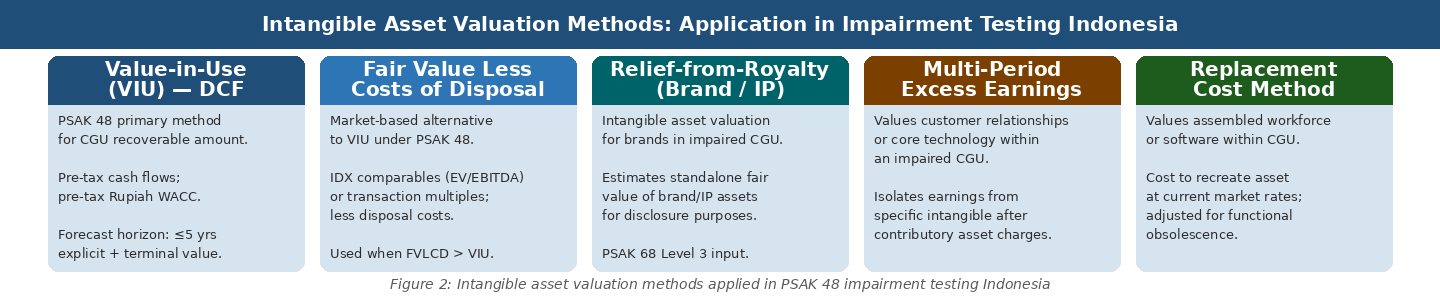

Methods of Intangible Asset Valuation in the Impairment Environment

In case an impairment indicator is applied in a CGU that includes both a tangible property and an identified intangible, such as a brand, customer relationship, technology platform, this recoverable amount should include the value of all the assets in the CGU, including the identified intangibles. In others, especially where recoverable amount is calculated by FVLCD, some special intangible asset valuation systems such as Relief-from-Royalty, Multi-Period Excess Earnings or replacement method of determining fair value of certain intangibles as part of the total CGU fair value should be used.

This is one of the most challenging technical parts of the PSAK 48 practice in Indonesia, as they need valuers who are knowledgeable both in IAS 36 / PSAK 48 impairment testing framework and in IFRS 13 / PSAK 68 fair value measurement of particular classes of intangible assets.

Figure 2: Intangible asset valuation methods applied in PSAK 48 impairment testing Indonesia

Why Impairment Testing Matters across Indonesian Industries and Reporting Contexts

The significance of using rigorous impairment testing Indonesia goes way beyond the technical PSAK compliance. It impacts all the stakeholders of the financial reporting environment, such as the management, auditors, investors, lenders, and regulators, and the implications of it are both financial and reputational.

Indonesian Balance Sheet Scale of Goodwill

The M&A market of Indonesia is more than 20 years old and over the years of operation, the market has been successful in creating cumulative goodwill balances that in the case of most of the listed conglomerates, constitute a considerable amount of reported equity. Where this goodwill is a real economic value, synergies realised, strategic positions secured, it is recorded in the balance sheet. It does not when it reflects the overpayment, unrealised synergies or degraded market positions. It is the impairment testing Indonesia which causes this distinction to be brought into the open and convenient fiction is substituted by disciplined measurement.

To the finance teams, boards and audit committees, goodwill line is among the most scrutinized figures in the financial statements. Massive accumulating balance of goodwill and regular purposely clean impairment test results raise the question whether the testing is rigorous or simply favorable to the capitalist version of management would prefer that the world should believe in. On the other hand, prompt recognition of impairment with clear disclosure of assumptions that informed the decision makes known the quality of governance and augments as opposed to diminishing management credibility.

Implications on the Investers and Capital Market

The quality of impairment testing is becoming a governance measure to institutional investors and equity analysts in Indonesia. Firms that build up goodwill without ever having to impair them, even though they are operating dismally, are regarded with increasing distrust. Once a significant impairment loss later becomes a reality, after years of seemingly clean testing, it usually initiates high-reaction share price reactions, investor confidence destruction, and examination of the financial reports of previous periods. This failure mode is prevented by the investment of learning how to impairment test Indonesia correctly, and within the first year of every acquisition.

OJK Regulatory Oversight

OJK prescribes that the Indonesian listed companies should give detailed disclosures on their testing of goodwill impairment, the CGU which the goodwill is assigned to, the basis on which the amount is determined to be recoverable (VIU or FVLCD), the key assumptions made, the discount used, the growth rates to be used in the projections, and the quantitative sensitivity analysis to indicate the effect of a change in the key assumptions. Corporations with generic, non-quantitative impairment disclosures or which revise assumptions between periods but do not disclose such revised assumptions, receive OJK enquiry letters and, in more severe instances, restatements.

Credits and Financing Implications

In the case of Indonesian firms having acquired debt financed goodwill, impairment recognition can create breaches of loan covenants where impairment was lower than levels stated in debt covenants. That is why impairment testing in Indonesia is not only a financial reporting issue, but also a liquidity and capital structure risk, which corporate treasurers and CFOs need to address proactively. The study of the connection between the impairment testing result and the covenant headroom is also included in mastering PSAK 48, in the Indonesian corporate environment.

Key Benefits of Mastering Impairment Testing Indonesia

Firms that treat impairment testing Indonesia as a governance practice, and not a compliance cost burden, continue to reap practical rewards in areas of financial reporting, investor relations, audit management, and strategic planning.

Balance Sheet Integrity

Early impairment recognition means that the reported assets had the true economic value that can be expected to be recovered by the business. Balances that reflect goodwill and intangibles at levels that cease to represent recoverable value are deceptive to investors and lenders- and will bring about an increasing disconnect between market capitalisation and reported book value which may ultimately be resolved by a large, disruptive impairment charge. This accumulation would be avoided through consistent, rigorous impairment testing which would identify the deterioration at its early stages and accurately reflect it in the financial statements.

Early Warning of Strategic Management

The annual impairment test involves the management reexamining the initial thesis of the acquisition which is the projections and assumptions that led to the premium paid against the actual performance of the business. When the recoverable amount has been found to have decreased towards carrying amount in the test, it gives a quantified early warning of the underlying business strategy, which the business might require a change. This is information management as would wish whether it prompts accounting charge or not. Firms that consider impairment headroom analysis a standing management reporting measure are always the first to spot strategic problems and respond in a better manner as compared to those who use the test as a pure reporting measure.

Efficiency in the Audit and Reduce Compliance Cost

Impairment testing engagements that had been put together with meticulous documentation of methodology, there were observable inputs of Indonesian market, pre-established sensitivity analysis and early concurrence by the auditor are reviewed much faster than those assembled in a hurry. The savings in management time and time taken by auditors to answer questions by the auditors can be measured as cost savings in a series of reporting periods. Finance departments that invest in learning how to do impairment testing using discipline annual procedures always report the lowest total audit friction levels when compared to departments that made decisions on managing the obligation on the fly.

Knowledgeable Mergers and Post Acquisition Integration

The discipline formed by the impairment testing structure goes back to the process of acquiring. Those companies familiar with the requirements of PSAK 48 on the CGU allocation requirements and the intangible asset valuation method that could be necessitated by the FVLCD calculation can better organize their acquisitions, negotiate purchase price allocation, and design a post-acquisition integration approach that maintains the economic value that created the acquisition premium. The art of mastering impairment testing Indonesia, otherwise, increases the quality of companies as acquirers.

Practical Applications: Impairment Testing Indonesia across Sectors

The issue of impairment testing is relevant to all types of the Indonesian economy, but the challenges and methods of analysis are highly diversified in different industries. The cases that are provided below represent trends that have been constantly observed in Indonesian financial reporting practice.

Case One: Mining Conglomerate – Commodity Price Trigger

A Jakarta-based mining conglomerate had purchased a nickel laterite processing project in Sulawesi and it realised IDR 1.1 trillion of goodwill in a CGU representing the processing plant and mining concessions. Global nickel prices fell significantly below the prices assumed in the initial acquisition model in the year after acquiring, and the result gave rise to a situation of accelerated impairment test in PSAK 48 before the year-end reporting date.

The impairment testing Indonesia team built a VIU model on consensus nickel price deck not the original optimistic assumptions, and assumed a five-year explicit outlook of cash flows, and a terminal value on a long-run real nickel price. The Indonesian risk-free rate of SBN 5-year yield was 16.2 and this was added to a mining sector risk premium, country risk premium, and asset-specific concentration premium of the single-facility CGU. This VIU of IDR 560 billion versus a carrying amount of IDR 1.32 trillion resulted in impairment loss of IDR 760 billion of which goodwill was written to zero and the remainder charged pro rata across the processing plant assets.

The sensitivity disclosure revealed that an increase in the nickel price in the long-run by 10 percent would have removed IDR 280 billion of the impairment. This sensitivity was prepared as with the main model build- not retroactively – as this way, the audit team could ensure the disclosure without some model revisions. The OJK took the disclosure at face value.

Case Two: Digital Platform Growth Assumption Challenge

A publicly traded Indonesian holding company had purchased a ride-hailing and logistics platform, with IDR 2.1 trillion of goodwill accounted to one CGU in which the operations of the platform occur in Java and Sulawesi. Three years after the acquisition, gross merchandise volume increased significantly but EBITDA was incredibly negative and the road to profitability was delayed several times in comparison with the management plan initially.

This was because the impairment testing Indonesia process needed VIU model to utilize projections that were justifiable through board given budgets and not aspirational management plans. The auditing firm questioned the fact that the five-year projections approved and which had assumed a sharp turn towards profitability in the second year was in line with the historical performance pattern of the business. The probability-weighted scenario method was finally followed: a central case with 50 percent weight that represented the trends in unit economics in the past, a management case with 30 percent weight, and a downside case with 20 percent weight. Goodwill impairment loss IDR 620 billion The probability-weighted VIU generated an impairment loss of IDR 620 billion on goodwill.

The important lesson of the case is that, in terms of high-growth, loss-making enterprises, PSAK 48 does not allow relying on aspirational projections, unless formally adopted by the board and in line with the past performance. The most effective thing is to involve the audit staff on projection methodology prior to the model development but not when the initial draft has already been criticized.

Case Three: Consumer Goods – Headroom Monitoring Governance

Five years ago, a group of consumer goods had purchased a regional snack brand, and they were aware of IDR 380 billion of goodwill. The CGU had passed annual impairment test in the five consecutive years that followed. Nevertheless, headroom analysis, which monitors the difference between recoverable amount and carrying amount, of the finance team revealed a steady decline: in the first year of the analysis, the team demonstrated a headroom of IDR 180 billion and in the final year, the analysis revealed IDR 42 billion of headroom.

A sensitivity analysis incorporated in the annual impairment testing process Indonesia in year five revealed that a 75-basis-point change in the WACC or a 5 per cent decline in estimated revenue would nullify all the remaining headroom and impairment would be triggered. This was the sensitivity that the finance department brought to the audit committee together with a strategic review recommendation. No impairment was recognised at that particular year and the business was repositioned and headroom reclaimed at later periods. The proactive application of impairment headroom analysis as a management tool; not a reporting output per se, had a direct impact on a strategic decision that saved asset value.

Case Four: Intangible Asset and Investment Property Impairment

A Surabaya-based retail group owned portfolio of shopping centre properties and substantial intangible assets, a retail brand and a loyalty programme customer base, which were identified in a preceding-year PPA. With physical retail footfall in the group catchment areas dropping in a structural manner, the finance department came to realize the impairment indicators of the CGU of the retail properties and other intangible linked to them.

PLCD as opposed to VIU was used to approximate the value recoverable because a hypothetical participant in the market will evaluate the CGU as being a group of commercial property resources and related operating companies. Direct capitalisation of net passing income was used to determine the values of the properties and it was adjusted to yield data that could be observed in similar Surabaya retail transactions. The valuation of the brand fair consisted of Relief-from-Royalty intangible asset valuation method, the customer base was MPEEM applied to the project net cash flows of the loyalty programme. The sum of FVLCD of IDR 1.84 trillion, less a carrying amount of IDR 2.21 trillion, yielded an impairment loss amounting to IDR 370 billion, and which was, firstly, recognized in goodwill (IDR 95 billion, written to zero), and, secondly, pro-rata on the other assets in the CGU.

Table 1: Impairment Testing Indonesia — Key PSAK 48 Requirements, Methods, and Indonesia-Specific Considerations

| PSAK 48 Topic | Requirement | Method / Approach | Key Indonesia Input | Common Error to Avoid |

| Goodwill testing | Annual, irrespective of indicators. | VIU (DCF) or FVLCD | SBN-based pre-tax Rupiah WACC | Application of USD rate as an IDR cash flow. |

| CGU identification | Smallest independent cash inflow group | Management reporting analysis. | Disclosures on the listing of segments of the IDX. | Combining weak + strong units to conceal the impairment. |

| VIU projections | Board-approved; not exceeding 5 years express. | Management accounts + DCF | IDR development rates; domestic price changes. | Aspirational unapproved forecasts. |

| FVLCD estimation | Exit price; or market participant basis. | IDX Comps or DCF + Disposal Costs. | IDX EV/EBITDA multiples + DLOM | The forgetting of DLOM of unlisted CGU. |

| Intangible asset valuation | FVLCD component fair value. | RFR, MPEEM, cost method | Indonesia royalties rate standards. | Nondisclosed intangibles FVLCD calc. |

| Impairment allocation | Good-will, and then pro-rata others. | NBV Proportional reduction. | Per-asset floor: max of 0, FVLCD, VIU | Inventory less than zero or own FVLCD. |

| Disclosure | CGU; approach; assumptions; sensitivity. | Table of quantitative sensitivity. | WACC; growth rate; price deck | Narrative, or part, where all measurements are generic. |

Source: PSAK 48 / IAS 36 requirements and Indonesian financial reporting practice.

Best Practices for Mastering Impairment Testing Indonesia

Auditors, independent valuation advisers, and finance professionals who have conducted several engagements to conduct tests of impairment in Indonesia all consistently find that there are a series of practices that distinguish between high-quality results and technically compliant, analytically weak results.

- Determine the appropriate level of granularity of CGUs at the date of acquisition – CGUs definitions must mirror the way management will oversee and produce returns, rather than how goodwill can best be impairment-free. Impairment that is to be recognised under PSAK 48 is obscured by overly broad CGU definitions that bring together profitable and underperforming businesses. The most important structural decision that can be made during every impairment testing programme is the clear and commercially defensible definitions of CGU at the time of acquisition (and review on a yearly basis).

- Always start with Rupiah-denominated WACC on first principles – the pre-tax discount rate applied in VIU calculations should reflect the Indonesian market conditions, which is built on the basis of the SBN yield as the risk-free base, the Indonesian equity risk premium, a sector beta based on those of companies listed in the IDX, and any size and specific-risk premiums. The use of a USD-based WACC on Rupiah cash flows without explicit currency adjustment is the most frequent reason of discounting the rates and overstating recoverable amounts in Indonesian impairment testing.

- Utilize board-approved projections and maintain a high level of rigor concerning the basis of such projections PSAK 48 holds that projections made by VIU must be based on reasonable and supportable assumptions that reflect the most appropriate estimate of the economic conditions over the remaining useful life of the asset. This would in practice imply that projections must be in line with formally board approved budgets and must be agreeable with historical performance. The impairment working papers of finance teams should include a multi-year forecast vs actuals is because it will be requested by the auditors and because the most frequent reason behind audit challenges to impairment test conclusions is unexplained forecast optimism.

- Sensitivity analysis should be built in the main model build, and not subsequent to it – PSAK 48 material goodwill CGUs should be disclosed quantitatively in sensitivity analysis. Writing this sensitivity table as a primary model, that is, testing the sensitivity of the impairment conclusion to realistic values of WACC, terminal growth rate, and the key operational driver (revenue, commodity price, occupancy) yield the quality output than retrospective sensitivity prepared under audit time pressure. It also confirms the major conclusion, in case small alterations of the assumptions do remove all the headroom, one has to take the conclusions with a grain of salt.

- Track impairment headroom as a statutory management report item – the difference between recoverable amount and carrying amount is not only an audit product, but a strategic risk indicator. Companies that monitor headroom on an annual basis, and report sensitivity-adjusted headroom to their audit committees, recognize diminishing CGUs earlier, act preemptively prior to impairment becoming unavoidable, and make disclosures that portray truly proactive governance, as opposed to compliance.

- Agree with the external auditors on methodology prior to the commencement of fieldwork – the most prevalent source of impairment test rework in Indonesia is a methodology disagreement between the audit team and the finance team, which becomes apparent after the model is created. Disclosure of the proposed CGU structure, derivation of discount rates, and projection basis to the audit team prior to the commencement of the actual modelling will eliminate most of these controversies before they spawn rework. This pre-fieldwork congruency is particularly vital to intricate CGUs that have several intangible asset appraisal techniques as part of the FVLCD calculation.

Common Challenges in Impairment Testing Indonesia and How to Address Them

Even well trained finance departments face a similar range of difficulties during the implementation of PSAK 48 impairment tests. It is these difficulties, and clear procedures of handling them that are what it actually takes to master impairment testing Indonesia.

Management Optimism of Forecasting

The quality of the cash flow projections that the VIU discounts is critical in terms of the calculation. The management forecasts in the Indonesian business culture, especially in family-owned or founder-led corporate culture, tend to have an aspirational but not probability weighted element. The effect of inaccurate projections that have historically exceeded actual performance by 2030% in three years do not constitute a reasonable and supportable foundation of a PSAK 48 VIU despite the belief of the management. Forecast reasonableness must be assessed by the auditors and the test of evidentiary standard is not merely qualitative but quantitative in nature.

The pragmatic resolution in this regard is to have a three-year forecast-versus-actuals analysis as a permanent part of the impairment testing working papers. In the case of a systematic overstatement of the forecasts, the VIU projections should be decreased or the sensitivity analysis should indicate the likelihood of poor performance. This analysis ought to be recorded on paper and shown to the audit committee; it shows the type of intellectual honesty that auditors need and that the shareholders should have.

CGU Restructuring to Avert Impairment

The temptation to reorganize CGU boundaries, to merge the poor performing CGU and profitable neighboring business, is a common issue in the practice of impairment testing in Indonesia when one acquisition is not performing. PSAK 48 allows CGU to make changes to boundary in cases where there is actual change in management monitoring, however, it should disclose the change and effect on accounting. The auditors are becoming more conscious of CGU restructuring as conveniently and conveniently coincides with the emergence of indicators of impairment and will question a change that seems to be aimed at sheltering goodwill as opposed to operational reality.

It will solve this by developing and formalizing a policy of definition of CGU to define the criteria on which CGU boundaries are identified and evaluated and to specify that any intended change should be reviewed independently by the internal audit or external counsel. This management structure is justifiable, and CGU management can be shown to be safe against any audit.

Valuation of Intangible Assets under the FVLCD Calculation

When the FVLCD is selected as the recoverable amount of a CGU which includes, among others, identified intangibles such as a brand, a set of customer relationships, a technology platform, valuing of the intangible assets should be performed by the finance department, to estimate the fair value of every element. This will demand competencies most of the Indonesian corporate finance departments have not cultivated internally: Relief-from-Royalty of brands, Multi-Period Excess Earnings of customer relationships and core technology, and replacement cost methods of assembled workforce and software.

The sensible answer is to involve the use of specialist valuation advisers who are proficient in both PSAK 48 impairment methodology and intangible assets valuation approaches mandated by PSAK 68. These two sets of skills do not overlap and the overlap of the two systems within one impairment test is what results in complexity that generalist advisers often underestimate. This need can be identified at an early stage, when the impairment test has not yet been done, to prevent the last minute scramble that creates high costs and low quality.

Disclosure Adequacy as per OJK Requirement

One of the most frequent reasons why OJK enquiry letters are sent to lists companies in Indonesia is because of generic disclosure and narrative only disclosure. PSAK 48 mandates, on each significant CGU that carries goodwill, the carrying amount of goodwill granted, the basis of determining the recoverable amount, the discount rate used, the growth rates, the period in which the projections are made and quantitative sensitivity analysis which illustrates that the key assumption would have to change to the extent that impairment would be recognised. Disclosures which do not provide all these elements, or to which disclosure only states that a test exists, and does not also include the necessary quantitative detail, do not pass the PSAK 48 standard or the disclosure expectations of the OJK.

Preparation of the disclosure note concurrently with the impairment model- not as a post-modelling exercise is the most effective protocol. Constructing the disclosure table as an output of the model will ensure that all the disclosure assumptions are exactly consistent with the value of the calculation and that the greatest head of disclosure-model inconsistency has been removed and that OJK-ready documentation is generated that can be filed without substantive amendment.

Conclusion: Mastering Impairment Testing Indonesia as a Finance Leadership Capability

Mastering impairment testing Indonesia PSAK 48 is not a technical success one time job but a discipline requiring following annual rigour, market awareness and governance adequacy also to make sure that the analysis is showing the reality and not the preference of the management. To financial reporting preparers in the corporate setting of Indonesia, including finance professionals, CFOs, audit committee members, and valuation advisers, PSAK 48 reflects one of the most significant requirements in financial reporting that integrates the difficulty of modelling discounted cash flows, intangible asset valuation methods, CGU-level of strategic evaluation, and regulatory disclosures into a single annual report.

The main principles, which at any rate constitute the practice of mastering impairment testing, in Indonesia, are similar in all fields and all types of companies: define CGUs properly and keep that definition disciplined; construct Rupiah-denominated WACCs using inputs to Indonesian markets; use board-approved projections able to be reconciled against historical performance; develop sensitivity analysis at the modelling stage not under pressure to satisfy auditors; measure impairment headroom as a strategic management measure; and prepare disclosures that meet the full quantitative requirements of PSAK 48 and the OJK.

The intangible assets valuation procedures that overlap with PSAK 48 when determining FVLCD- Relief-from-Royalty, Multi-Period Excess Earnings, replacement cost are not peripheral to the Indonesian impairment. To companies that have undertaken acquisitions and reflect substantial identified intangibles on their balance sheets, such methods are a necessary constituent of a full and conforming impairment test. Finance teams that invest in building such a set of combined skills, PSAK 48 methodology plus the intangible asset valuation methods of PSAK 68, will be much better equipped to meet the challenges of the audit, the expectations of investors and regulatory obligations that characterize Indonesia emerging financial reporting environment.

The economy of Indonesia has continued to give birth to acquisitions, purchase countertransactions in the capital markets and goodwill that comes with the same. The firms and practitioners who learn how to impairment test Indonesia not as a compliance study but as a true governance skill will now report with a higher degree of believability, they will exercise greater disciplines of their assets and will also have confidence to withstand the inquiry of the advanced investors and regulators in years to come.