Common Valuation Errors Before Sale

The decision to sell a business is also one of the most impactful financial occurrences that an owner or an executive will go through. Regardless of whether the deal is between a mid-market manufacturer company, a regional logistics service or even a high-growth technology company, the valuation exercise is at the centre of the deal. But, nonetheless, valuation is among the most mismanaged processes in the pre-sale procedure. Mistakes committed during this phase may lead to deal failure, proceeds which are far below what was projected, or post-close disagreements which drag on and on.

In the case of junior or mid-level members of the finance department; the analysts, associates, and corporate finance managers who are dealing with sell-side transactions on the first time, knowing the areas where valuations fail is as informative as knowing how to create a valuation that works. The paper is a step-by-step explanation of the most prevalent errors in the process of business valuation, with each example being accompanied by real-life examples and provided with the sensible guidance on how to prevent them. It also describes the best practices in company valuation that ought to make themselves a second nature as an individual practitioner who may be keen to provide credible results that can be defended.

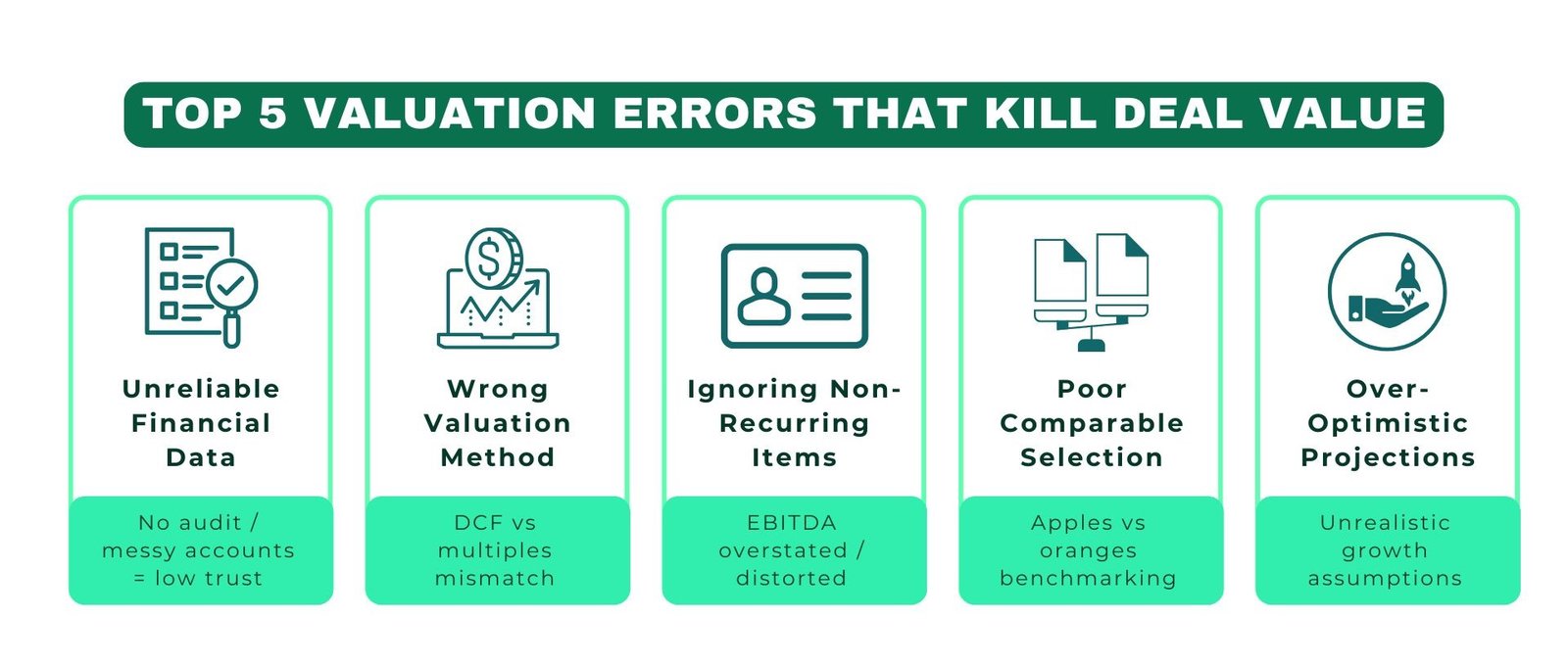

The process of valuation is not a one-time calculation, but a stratified process which relies on financial modelling, market instincts, industry experience and strategic background. The pitfalls that business valuation professionals have to avoid are generally structured around five categories, namely the use of financial data that is not high quality, the inappropriateness of the methodology applied, the treatment of non-recurring items, the identification of similar companies or transactions, and the treatment of forward-looking assumptions. All these are expounded below.

Picture 1 : Top 5 Valuation Errors that Kill Deal Value

Starting With Unreliable or Unaudited Financial Data

Picture 2 : Pre-Sale Valuation: Best Practice Workflow

Among the most widespread typical errors in the business valuation process, one can distinguish initiating the process with the financial statements that were not reviewed or audited properly. In certain cases, especially with the private firms, management accounts are in most cases prepared to be used in making decisions within the firm, as opposed to being opened up to external auditing. These pronouncements might consist of conflicting categorization of costs, the unofficial recognition of revenues, or expenses incurred by the owners that are enclosed in the operations framework of the business. Once these figures are the basis of a valuation, what comes out is a figure that can be disputed by any intelligent buyer, and disputed successfully.

Look at an example of a European specialty chemicals distributor that presented three years of management accounts and no audited financial reports to the market. Those internal numbers were healthy EBITDA multiple, which the investment bank of the seller pegged the valuation. In their due diligence, the buyer consultants found out that the family salaries of the owner consisting of more than EUR 800,000 per year were partly expensed as operating costs, instead of distributing to the owner. After these were rightly categorized and the EBITDA was recalculated, the negotiated enterprise value reduced by almost a fifth. The moral of this story is simple enough the better the inputs, the better the outputs are credible.

The ideal practice in the company valuation is that sellers are supposed to have best practices by commissioning independent quality of earnings (QoE) report prior to going to market. The financials are normalised and one-off items identified in this document prepared by an independent accounting firm and adjusted EBITDA are presented in a form that will be accepted by buyers and their advisors as valid. Sellers that undertake this step will normally undergo a less arduous due diligence process, a reduced number of valuation renegotiations and in the end gain higher proceeds.

Process Flow 1: Before Valuation Financial Data Preparation.

| Step | Action | Responsible Party | Output |

| 1 | Prepare 3-5 years management accounts. | CFO / Finance Team | Raw financial data |

| 2 | Determine non-recurring costs and those of the owner. | CFO + External Advisor | Adjustment schedule |

| 3 | Commission Quality of Earnings (QoE) report | Independent Accountant | Normalised EBITDA |

| 4 | Make financials match selected valuation methodology. | Investment Bank / Advisor | Adjusted financial model |

| 5 | Introduce in data room to prospective customers. | M&A Counsel / Banker | Buyer-ready financials |

Selecting the Wrong Valuation Methodology

The other group of common pitfalls in business valuation takes place due to the application of a methodology that is not appropriate to the business under valuation. It is possible to identify three main approaches to it, namely the income approach (discounted cash flow), the market approach (comparable companies or precedent transactions), and the asset approach, and each of them has its proper context. Using a DCF on a business that has highly volatile or unpredictable cash flows such as one may result in a large and ultimately useless valuation range. Equally, the asset approach applied to service business where there is limited tangible assets to the business will undervalue it systematically.

An example that is helpful is in the healthcare services industry. In the United Kingdom, an outpatient clinic organization financed by a private equity company was taken to market by a pure DCF approach. The cash flows within the business were very high in the previous years, and the forecast period was also the same with the anticipated changes in NHS policy that brought about an element of uncertainty to the revenue forecasts. To deal with this uncertainty, buyers used a larger discount rate to discount the value yielded by the DCF thus lowering the value significantly. The sell-side advisors made it worse by not cross-referencing their DCF with a similar transactions analysis, which would have indicated that similar clinic operators have recently traded at much greater EV/EBITDA multiples in the open market.

To prevent such a type of typical errors in business appraisal, it is necessary to pick such methodology or rather a combination of the methods that best represents how the buyers in that particular industry actually price transactions. A combination of DCF and market multiples triangulation presents an outlook and a reality check in the market to most operating businesses. The advisors must be always ready to justify and defend their choice of methodology to the prospective buyers because it is the credibility that provides the basis of the whole valuation story.

Table 1: Valuation Methodology Selection Guide

| Business Type | Recommended Methodology | Key Metric | Limitation |

| Stable operating business | EV/EBITDA Comparable Multiples | EBITDA | Bases on similar availability of deal. |

| High-growth technology company | DCF / Revenue Multiples | ARR / Revenue | Sensitive to terminal value presumes. |

| Asset-heavy manufacturing | Asset Approach + EV/EBITDA | Net Asset Value | May understated value in terms of intangible. |

| Early-stage startup | Venture Capital/ Scorecard Method. | MRR / User Growth | Highly subjective |

| Financial institution | Price-to-Book / P/E | Book Value | Limited cross-sector comparability |

Failing to Identify and Adjust for Non-Recurring Items

One of the most technically harmful of the pitfalls of business valuation is the inability to get the non-recurring items out of normalised earnings in a proper manner, as the cost involved is both frequent and expensive. Items not recurring are expenses or revenues that are occasioned by an event that is unlikely to occur in the normal operations of the business. These are the restructuring charges, settlement of litigation, a single time consulting fees, moving premises, or the revenue of a discontinued contract. When these items are not accommodated the EBITDA that is used in the valuation will be skewed and give a multiple that does not reflect the underlying true profitability of the business.

Of course, the difficulty is that the boundary between the recurring and non-recurring is not always visible. A business may claim that a certain legal fee was an isolated incident where the accountant of a buyer may indicate that the business has paid the same fee in three out of the five years that it has been in operation, which implies that it is not an exception but an inherent aspect of the cost base. It is precisely this type of dispute that destroys trust between the buyers and the sellers in the process of due diligence and destroys transactions altogether.

At best practices in company valuation, there are five important steps that are based on the management of non-recurring items:

- Line by line analysis of profit and loss account over a period of three or five years to determine things that seem out of place in terms of timing or quantities.

- Have all the suggested changes documented with a clear explanation and a support of evidence, i.e. board minutes, legal correspondence, one-time invoices

- Compare and adjust to industry standards to be able to justify the procedures by referring to how other companies of the similar type organize their cost base.

- Stress-test the adjusted EBITDA by taking the case of a buyer refusing one or two of the suggested adjustments, to find out the extent to which there is pricing space.

- Disclose the adjustments in the information memorandum and there should be a clear bridge between the reported EBITDA and normalised EBITDA to enable the buyers to follow the logic and not to need to interpret it on their own.

These steps will not make buyers agree to all the changes, but it will make sure that the position of the seller is logical, written, and presented professionally, which will minimize the possibility of conflicting renegotiations in the future of the process.

Using Poor or Mismatched Comparable Companies

It is the choice of peer companies and past transaction that are subject to common business valuation error that can lead to subtle distortion of results that cannot be easily identified without extensive knowledge of the industry. The market approach principle is simple; when similar businesses have been sold at specific multiples, such multiples would give a market derived benchmark to the business under valuation. The problem is that it is difficult to define similar. Geographical variations, business model variations, scale variations, customer concentration variations, contract structure variations, and growth profile variations are all valid grounds to have material differences in multiple – and this is where it is important to be wrong, either way, this will invalidate the whole exercise.

The case of the business process outsourcing (BPO) provider located in Eastern Europe can be discussed. The sample of the sell-side advisor consisted of a peer group consisting of a number of large-cap BPO companies listed on big stock markets in the United States and India. The revenues of these businesses were five to ten times higher than the one under valuation, had dozens of geographies and had installed technology platforms, which were able to produce recurring software revenues on top of the services fees. The multiples used on these characteristics were significantly high compared to those that were suitable to a smaller and geographically oriented business in terms of services. This ensuing overpricing resulted in a painful revaluation in the due diligence, and would eventually result in the first buyer backing out.

The best practices in company valuation in this field involves creating a peer group that emphasises on the similarity in operations and structure as opposed to categorising the sector. Advisors are expected to explain the rationale of the inclusion of every similarity and in instances where there are variations, they should make clear multiple modifications with justifiable explanations. In cases where the public similar set is sparse or ill-matched, precedent private transactions (where databases of such as Mercermarket or PitchBook are available) may be a more appropriate reference point than data on the public market.

Table 2: Evaluation Criteria Used to Measure Similar Companies.

| Criteria | What to Assess | Red Flag of being mismatched. |

| Revenue Scale | At a range between 0.5x-2x target company revenue | Implied multiples are inflated by large cap comps. |

| Business Model | Services, product, SaaS, hybrid. | SaaS multiplies that are used improperly on pure-services companies. |

| Geography | Same or neighbouring regional market exposure. | US/EU multiples applied wrongly on the emerging markets. |

| Growth Profile | Equal growth rate (±5% CAGR) of the company. | Comp growth High growth alters value of mature business. |

| Customer Concentration | Like major key customer risk exposure. | Concentrated revenue is overvalued in diversified comps. |

Over-Optimistic Forward Projections and Assumption Creep

The common pitfalls in business valuation is perhaps the inflation of future projections. The sell-side is inherently a tension where the sellers and their advisors are interested in making the best case scenario, and buyers and their advisors are conditioned to be sceptical of any forecast being made by the party possessing the most financial incentive to have a positive future performance. As soon as the projections are not based on the historical performance, or realistic market data, this strain breaks, and the valuations based on these projections are instantly called into question.

An example of real-world based on this is the retail consumer goods. One of the mid-sized branded goods companies in Scandinavia had provided a five-year revenue prognosis, which presupposed a compounded yearly growth of 22, even though the company had been expanding at the average of 7 percent over the past four years. Scheduled geographic expansion into three new markets as well as the introduction of two new product lines were in the forecast, but they lacked a record of implementation behind them, something which although not impossible, was not likely to happen. The values of the implied enterprise value fell by almost 35 percent when the analysts of prospective buyers took the model to the stress test with a base case assumption that maintained the growth at the historical rates. The deal was finally to transact at a price much lower than the expectations of the seller.

This is an intellectual issue to deal with this risk. The best practice in the company valuation would require projections that are clearly linked to previous performance, which is backed up by recorded assumptions and are stress-tested in various situations. The advisors also ought to be upfront with their clients on the distinction between a strategic aspirations and a financial projection. Being able to include a base case, an upside case and a downside case in the information memorandum, rather than provide a one-sided scenario of optimism, in fact, causes credibility amongst buyers since it shows analytical rigour and realism.

Flow Process 2: The Pre-Sale Valuation Review Process.

| Phase | Activity | Key Output | Timing (Pre-Sale) |

| Phase 1 | Hire M&A consultant and establish scope of valuation. | Involvement letter and project planning. | 12–18 months prior |

| Phase 2 | Commission Quality of Earnings Report. | Adjustment schedule and normalised EBITDA. | 10–14 months prior |

| Phase 3 | Develop financial model and methodology test. | Scenario analysis Valuation range. | 8–10 months prior |

| Phase 4 | Detect and filter other similar companies/transactions. | Peer group and multiple range are both validated. | 6–8 months prior |

| Phase 5 | Make preparations of information memorandum and projections. | Base/upside/downside cases of IM buyer-ready. | 4–6 months prior |

| Phase 6 | Pre-diligence internal audit. | Solved information voids and documentation package. | 2–4 months prior |

Conclusion: Actionable Insights for Valuation Practitioners

Prejudices made prior to a sale are not caused by ignorance very often, but rather by optimism, time pressure or the inability to exercise consistent professional discipline throughout the process. The pitfalls of business valuation identified in this paper include unreliable financial information, misplaced methodology, non-recurring items, poor choice of comparable and overstated projections and all these are points where the rigour can be lost and the value could be destroyed.

In the case of practitioners in the corporate finance, investment banking or advisory business, the lessons learned are practical. The first step is to invest in the quality of the financial data that is to be used before any valuation work is done. Second, choose a methodology that shows the way the market values the businesses of the considered industry. Third, do so in a disciplined manner in terms of normalising earnings, and the documentation should be able to be scrutinised. Fourth, create a peer group which is really similar, not just convenient. And fifth, projections onto historical reality and it should also be clear about the assumptions in each scenario.

The best practices in company valuation is not an imaginary concept, but it is rather the practices and traditions of successful advisors who seal a deal at target prices as opposed to advisors who take months to run a process that falls under due diligence. The prevention of the common pitfalls in business valuation is all about credibility: the credibility of the figures, the credibility of its analysis, and credibility of the team presenting them to the market. Customers are not that naive and they will put to test all the assumptions. The sell-side professionals who is best suited to withstand that type of scrutiny will be the one who has already posed the most difficult questions to himself – and answered them honestly – prior to going to market.