Step-by-Step Guide to Impairment Testing MFRS 136

A Practical Guide for Valuation and Finance Professionals in Malaysia

Introduction to Step-by-Step Guide to Impairment Testing MFRS 136

The goodwill and other long-lived property do not necessarily decrease in an accounting system, such a decrease has to be determined, quantified and registered in a formal manner, through a well-organized process. That is regulated by the local version of IAS 36 (Impairment of Assets), MFRS 136, in Malaysia and it is one of the most technically challenging undertakings a finance or valuation specialist will face. To most listed Malaysian firms, the Malaysia cycle of the annual impairment testing is not just a compliance exercise but rather a substantive valuation exercise, potentially capable of shifting earnings, influencing the credibility of the balance sheet, and attracting considerable scrutiny by the auditors, the Securities Commission, and the investment community.

MFRS 136 is a poorly comprehended practitioner level at its relevance. The difference between what the standard specifies and what is actually provided in management accounts and audit support packs is even greater than most professionals would admit. Some of the common weaknesses are that the boundaries of the cash-generating units (CGU) are too vaguely defined, terminal growth rates are not supported by economic data, and discount rates that mix pre-tax and post-tax input. These are no trivial technical lapses, they are producing audit results, necessitate financial restatements and, in the case of IFRS compliance in Malaysia valuation, an underlying misuse of the fair value measurement concepts the standard is based on.

This paper takes one through the impairment testing procedure on a first principles basis, taking MFRS 136 as the guideline and based on the practical experience in Malaysian engagements. It is composed with junior to mid-level professionals who may be faced with impairment testing first time, or those who may be in the process of developing their skills. It also applies to individuals working in the field of business valuation Malaysia and advisory practices, where impairment work is a frequent occurrence in conjunction with PPA Malaysia exercises that occur after mergers and acquisitions.

Understanding the Purpose and Scope of Step-by-Step Guide to Impairment Testing MFRS 136

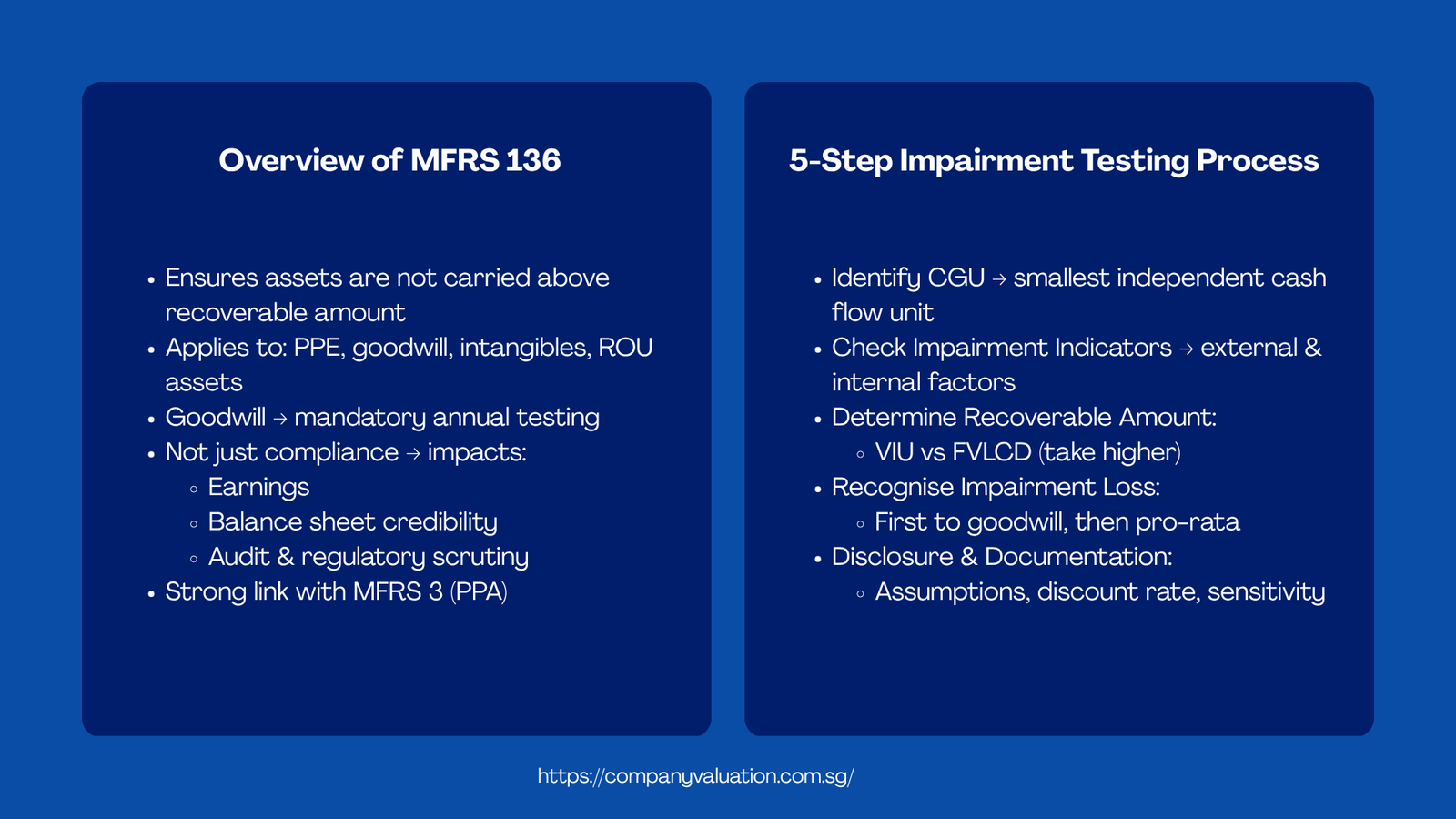

Fundamentally, MFRS 136 was created due to the need to make sure that assets do not appear in the books of a company at values that are above their recoverable amount; the higher between the amount an asset would fetch when sold, less the cost of disposing of the asset, or the amount the asset would fetch when used. The standard is general: to property, plant and equipment, right-of-use assets, intangible assets and goodwill that are a result of business combinations. It is not applicable to inventories, financial instruments, or deferred tax assets, all of which are subject to different standards, and have different impairment models.

Goodwill is the most important category under MFRS 136 in the Malaysian context. All companies that have experienced a business combination have goodwill on the balance sheet which has to be test annually without consideration of whether an impairment indicator has arisen or not. This is a very important difference compared to other asset classes, which are tested only when a trigger event happens. This means that the impairment testing Malaysia work is not an episodic work, it is a part of the financial reporting cycle and should be resourced and planned as a repetitive exercise, rather than being an afterthought at the end of the year.

It is also necessary to understand the connection between MFRS 136 and MFRS 3. In a case where a company acquires another company, the PPA Malaysia exercise under MFRS 3 stipulates the way the purchase price is to be divided into identifiable assets, liabilities and residual goodwill. Such an allocation directly influences the CGU structure applied in each further impairment test. Inadequate purchase price allocation work – such as the inability to separately determine customer relations, technology assets or trade names – generally overstates the balance in the goodwill and renders the subsequent impairment testing to be more material and more challenging to justify. The two exercises are highly connected, and mistakes in one are bound to be transferred to the other.

The 5 Step Impairment Testing Process | Step-by-Step Guide to Impairment Testing MFRS 136

The technical implementation of an impairment test is a process that needs discipline and is carried out in a sequence. Five basic stages that are the subject of consideration in the table below, what each of them entails in practice and what particular provisions of MFRS 136 govern them. To practitioners building their competency in impairment testing Malaysia, quality work begins with the treatment of this as a workflow as opposed to individual calculations.

| Step | Stage | What You Do | MFRS 136 Reference |

|---|---|---|---|

| 1 | Identify the CGU | Establish the smallest identifiable pool of assets producing the cash inflows which are mostly independent. Matching CGU boundaries to management reporting lines and operation structure. | In paragraph 6, the definition of a Cash-Generating Unit (CGU) and the criteria used in identifying one are given. |

| 2 | Identify Impairment Indicators | Examine market decline, increasing rates, regulatory changes external, and operate losses, asset degradation internal. Goodwill and indefinite-life intangibles are to be tested annually without any indicators. | Both external and internal signs of impairment are discussed in paragraphs 9 to 17. |

| 3 | Determine Recoverable Amount | Assess Value-in-Use (VIU) and Fair Value Less Costs of Disposal (FVLCD). Of the two, the larger amount is recoverable amount. Do not fail to VIU without looking at FVLCD. | According to paragraph 18, the recoverable amount is the greater of Fair Value Less Costs of Disposition (FVLCD) and Value in Use (VIU). |

| 4 | Recognise and Allocate Impairment | In case recoverable amount is less than carrying amount, impairment loss should be recognised. The first to goodwill and pro-rata to other assets in the CGU. It is not possible to write assets at lower amounts than they can be recovered. | Paragraph 59 and 104 deal with the recognition and allocation of impairment losses. |

| 5 | Disclose and Document | Make financial statement disclosures of major assumptions, terminal growth rates, discount rates and sensitivity analysis. Keep work papers which connect assumptions with approved budgets of management. | The disclosure requirements associated with impairment testing are contained in paragraphs 126 to 137. |

It is in steps 1 and 2 where the most consequential judgments are done but they are the least addressed in most engagements. In this case, specifically, CGU identification defines the whole architecture of the test. A CGU which is too broad-based will blur impairment on an individual asset basis; one which is too narrow will result in artificial triggers which are unrealistic of operational reality. The guideline of the standard that a CGU is a smallest set of assets producing significantly independent cash flows sounds easy, however, it needs actual knowledge of the working of the business to be exercised with honesty.

The next step (2) should be given purposeful consideration every year as well. Although, even with a goodwill requiring annual testing, a practitioner must still determine whether impairment indicators exist at the asset-level, as this impacts on when and how other asset classes should be tested within the same CGU. The weaknesses in the documentation of impairments in Malaysia are constant as the indicator assessment is treated as a checkbox exercise, as opposed to an actual review of the business environment.

Calculating Recoverable Amount Using VIU and FVLCD | Step-by-Step Guide to Impairment Testing MFRS 136

The recoverable amount calculation is the core of any impairment test, and the decision between Value-in-Use (VIU) and Fair Value Less Costs of Disposal (FVLCD) is not a matter of style rather than it can dictate the occurrence of impairment charge altogether. Most companies in the practice of the Malaysian default to VIU due to the ease of access to the management cash flow projections compared to the market transaction data. Nonetheless, there is a risk to this default: in cases where FVLCD would generate a greater recoverable amount, it is not a conservative position, but it is a non-compliant position that overstates the impairment charge.

| Criteria | Value-in-Use (VIU) | Fair Value Less Costs of Disposal (FVLCD) |

|---|---|---|

| Definition | Future cash flow of the continuity of future use and ultimate disposal of the asset or CGU on the basis of present value. | Price that is attained through a sale of the asset in a systematic transaction among the market participants with the exclusion of the estimated disposal costs. |

| Best Used When | The property is part of current business and the organization will not sell it but will keep on using it. | There is an asset or CGU market; in case FVLCD surpasses VIU, it can avoid recording an impairment charge. |

| Key Inputs | Projected cash flow of management (within 5 years), terminal growth rate, and pre-tax WACC as the discount rate. | The market transaction prices, similar sales evidence or a DCF estimated at the perspective of a market participant (in line with MFRS 13). |

| Common Pitfall | Basing management projections on aspirational targets and not consistent assumptions that are supported by the market. | FVLCD has not even been considered, even though it might lead to a greater amount of recoverable amount – a non-compliance risk under MFRS 136. |

| Standard Reference | The paragraphs 30-57 are used to control the cash flow projections, extrapolation period, growth rates, and derivation of discount rate. | Paragraphs 25-29 present the fair value measurement with reference made to the MFRS 13 (IFRS 13) to provide the measurement framework. |

An example of this tension is in the Malaysian plantation industry. The VIU of a mid-sized agribusiness with a high goodwill after a preceding takeover was plummeted after many years of low commodity prices. The finance team which was fully dedicated to VIU determined that a material impairment charge was needed. An objective audit later pointed out that the underlying plantation land had increased in value considerably and that FVLCD which was pegged on recent sales of similar plantation land in Sabah was significantly higher than the carrying amount. The right thing to have done was to calculate both the measures and realise the larger number such that an impairment charge would have been technically wrong.

Another broader principle that is shown in this case and that forms the basis of the IFRS valuation Malaysia practice is that standard does not assume companies to take the most conservative position but the right one. The reason why recoverable amount is determined as the greater of two items is that value can be realised in various ways, and an asset should not be written down in instances where there is a realistic basis of genuine carrying amount. To practitioners, the art of computing VIU and FVLCD even when one is supposed to prevail is technically necessary and professionally good.

Calculation of the Discount Rate | Step-by-Step Guide to Impairment Testing MFRS 136

Among all the inputs of a VIU calculation, the discount rate is the most sensitive and it is the one that will face the most scrutiny over time by auditors and peer reviewers. The input also is the most directly related to the quality of the judgment of the practitioner in the context of business valuation Malaysia. MFRS 136 provides a pre-tax discount rate based on current market judgments of the time value of money and risks unique to the CGU, in practice a pre-tax weighted average cost of capital (WACC) composed of elements each backed by observable market data.

| Step | Component | How to Derive It (Malaysia Context) | Typical Range / Note |

|---|---|---|---|

| 1 | Risk-Free Rate | Employ yield of Malaysian Government Securities (MGS) which has the same maturity as the projection period. The most popular benchmark is the 10-year MGS yield. | About 3.8 per cent. to 4.2 per cent. during recent periods. Refreshing of every testing cycle – do not transfer rates of the past years without examination. |

| 2 | Equity Risk Premium | Obtain based on known financial databases on Malaysia, or based on past Bursa Malaysia returns on equities in terms of the risk-free rate. Calculate a country risk premium to emerging market exposure. | Total ERP Malaysia Uncharacteristic of country risk premiums. Record source and date of the used data. |

| 3 | Beta | Minimum of 100 listed peer companies in Bursa Malaysia or other similar markets. Unleverage the beta of every peer and leverage the capital structure of subject CGU. | Malaysian industries Unlevered beta of 0.5-0.9. It is best to avoid a single peer; five or more peers are better. |

| 4 | Size and Specific Risk Premium | Introduce a size premium to smaller, less liquid businesses. Where the CGU involves idiosyncratic risks that are not reflected by systematic beta key-person dependency, customer concentration add a premium that is specific to the company. | Size premium: 1%–3%. Case-specific risk premium is a case-specific risk premium, which has to be justified and reported individually. |

| 5 | Convert to Pre-Tax Rate | The MFRS 136 will predetermine the application of a pre-tax discount rate on the pre-tax cash flows. WACC: In case WACC is computed after taxation, gross up: Pre-tax rate = Post-tax rate/(1-tax rate applicable). The current corporate tax rate is 24 percent in Malaysia. | This is an approximation of the conversion. An iterative method can be suitable in complex tax profiles. Discuss and discuss with your audit reviewer. |

Step 5, conversion before tax, is one area where there has been continued inaccuracy in Malaysian impairment models. Most practitioners are calculating their post-tax WACC (which is methodologically correct), and then gross them up before applying them to pre-tax cash flows. The identification of this inconsistency in audit inevitably necessitates reworking, and may cause a shift in the amount recoverable of material magnitude. The grossing-up formula is a roughness, and in the case of a complex tax profile of a business, including deferred tax asset, pioneer status incentive, or a difference in rate between operations, a stricter iteration should be considered. It is an indication of professional maturity to be explicit about this choice in your workpapers, and to note it as something you would discuss with the audit team.

What needs more attention than it is usually given is the derivation of beta. In the case of a Malaysian subsidiary or a conglomerate division or a personal company in impairment testing, choosing peer companies in Bursa Malaysia may not give a strong sample of the companies, especially in a niche or specialist industry. Comparables in the region such as Indonesia, Thailand, or the Philippines are usually suitable, although differences in leverage, size and market conditions must be adjusted. Its goal is a beta, which captures the systematic risk of the operations of the CGU, not the risk of the group as a whole, and not a figure that has been drawn out of a database without any examination of the composition or currency of its underlying components.

Audit Readiness, Disclosure and Documentation | Step-by-Step Guide to Impairment Testing MFRS 136

Technically sound impairment test which has not been documented well is, technically speaking, almost as bad as the one that has not been done at all in the view of the audit. MFRS 136 puts very specific disclosure requirements and the quality of the disclosures, both in the financial statements and in the work-papers, will reflect to the reviewers how seriously the exercise has been taken. To practitioners developing an impairment testing practice in impairment testing Malaysia, it is as vital to learn what the auditors and regulators actually review as it is to learn the technical mechanics.

| Disclosure Area | What MFRS 136 Requires | What Auditors Typically Challenge |

|---|---|---|

| Key Assumptions | Present the foundation of each of the major assumptions: growth rates of revenues, margins, and capital expenditure amounts, as entered into the cash flow model. | Assumptions that are not in line with the approved budget set by the board or past trends of performance without explanation. |

| Terminal Growth Rate | Stated terminal growth rate used to extrapolate cash flows past the detailed forecast period and justify. | Rates more than the long-run nominal GDP or sector growth with no industry data or management explanation. |

| Discount Rate | Report the pre-tax rate on the CGU, or the post-tax rate (where post-tax cash flows are being used) and briefly explain how it was calculated. | Post-tax rates on pre-tax cash flows; rates which are low in comparison with visible market rates or peer-based estimates of WACCs. |

| Sensitivity Analysis | Regarding the material CGU, disclose reasonably possible changes in the key assumptions that might result in carrying amount of the material CGU being equal to the recoverable amount. | Tables of sensitivity that are not present at all, or that indicate implausibly large headrooms with no subsequent stress testing of assumptions. |

| Basis for Recoverable Amount | Indicate the basis of recoverable amount VIU or FVLCD and explain how this is measured, with what methodology. | Omission in taking into account FVLCD in the case of a disposal market; inadequate description of how the valuation will be done to support audit trail. |

One of the requirements of MFRS 136.134(f) that most companies have dealt with loosely is the sensitivity disclosure requirement. The standard evidences entities to report the amount in which the recoverable amount would have to vary, or the material assumptions would have to change, in order to have the CGU carrying amount reflect its recoverable amount. It is a material message to shareholders on headroom and fragility. A sensitivity table which shows an enormous margin of safety with no contextual discussion is almost as useless as a sensitivity table which is not included at all. Sensitivity disclosures are increasingly required by auditors to represent truly reasonable situations rather than the calculation to demonstrate that no impairment can possibly occur.

In the case of junior practitioners, the most convenient habit to be made is to trace every major assumption of the impairment model to a written management source: the board-approved budget, the latest strategic plan, or industry information of a named external source. Audit findings that are yet to occur are inconsistencies between the impairment model and management reporting, such as the projection of 15% revenue growth in the VIU, and 5% in the board budget. Having that connection in your workpapers and being capable of explaining that connection under questioning is not only a quality control factor but a professional distinction feature that your seniors and audit teams will be aware of.

Conclusion : Step-by-Step Guide to Impairment Testing MFRS 136

The MFRS 136 impairment testing is one of the most technically challenging recurrent procedures in the financial reporting and the process where the quality of the underlying work, the CGU definitions, the cash flow projections, the derivation of the discount rate and the disclosures, have direct impact on the credibility of the financial statements. To business valuation practitioners, business valuation advisors and to the in-house business finance team, building authentic skill in this field is one of the most valuable investments one can make at any stage of career.

The lessons learnt are practical. A cautious definition of CGU should always be started with, as it will define everything below. Calculate VIU and FVLCD both and record the reason you have used the higher, not the more convenient. Derive your discount rate on first principles, specify the conversion of this into after tax, and refresh all elements with each test cycle. It is also important to bear in mind the relationship with PPA Malaysia: any impairment test that you make is in some way a by-product of the purchase price allocation decisions that you make and more rigourous your PPA today, the less complex is the impairment in the next reporting period.

The practitioners who create the most justifiable impairment work in the wider IFRS valuation Malaysia are not those who are most familiar with the standard in its abstract form but those who are able to apply its principles in a well-grounded, well-documented, and commercially-based analysis. It is that blend of technical knowledge and practical judgment that has been acquired with conscious exposure to the standard and with the real world engagements that is eventually what impairment testing under MFRS 136 requires and rewards.