Professional Business Valuation Report Services Indonesia

Introduction to Professional Business Valuation Report Services Indonesia

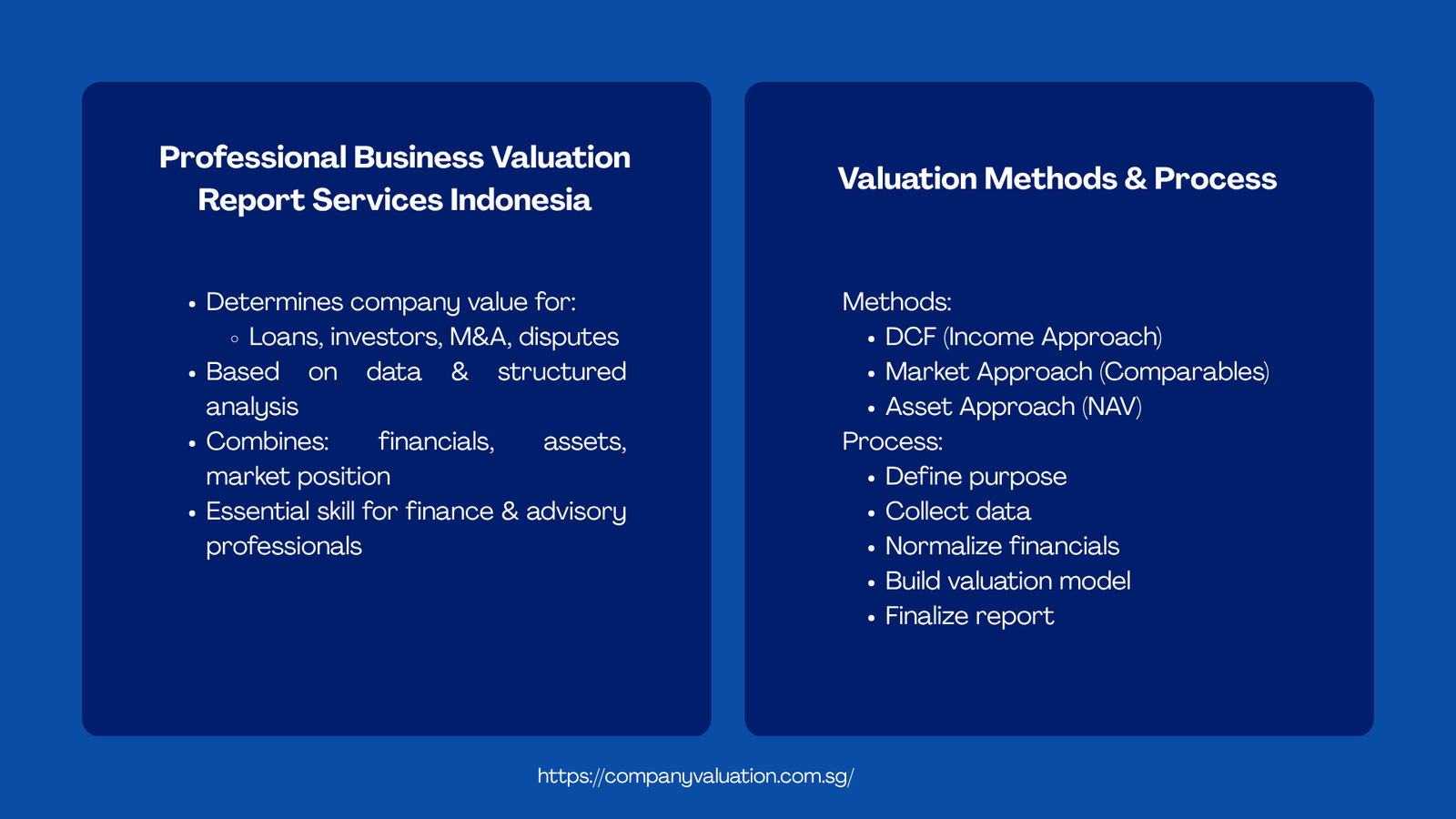

Every big business operation in Indonesia, be it seeking a bank loan, attracting foreign investors to invest in a business, a merger or even a shareholder brawl, is premised around a question: what is the value of this company? That solution is seldom intuitive or spreadsheet calculations. It is anchored on a professionally prepared Indonesia business valuation report, a systematic, evidence based report, where the financial performance of a business, its asset base and competitive position are translated into a value number that is attainable.

The manner in which these reports are structured and what renders them believable is a competency core to the professionals who come into the ranks of corporate finance, investment advisory or management consultants in Indonesia. Increased and dynamic economic growth pace and also increasing regulatory examination of the nation by Otoritas Jasa Keuangan (OJK) and the Directorate General of taxation has led to the high and ever-increasing demand of business valuation Indonesia services which can not only meet the local regulatory demands but also the global best practice.

This paper will take you through the basics of Indonesia business valuation services: how this is done, what the process entails, what real engagements usually entail and what junior professionals should remember to keep in mind as they develop competency in this field.

Relevance of Professional Business Valuation Report Services Indonesia

Indonesia is a unique stratum of businesses. Most industries have family owned conglomerates and the publicly traded companies and technology startups that are on a steep ascendancy. This diversity means that the valuation professionals are faced with a wide range of forms of engagement – which are different regarding the expectations of the stakeholders, quality of data, and regulatory requirements. When a valuation of a fast-moving consumer goods (FMCG) company in Jakarta is being considered with a view to finding a private equity partner, this type of valuation seems distinctly different than a manufacturing company in Surabaya and undergoing a tax audit.

Independent valuation report Indonesian Financial Services Authority (OJK) is a requirement where certain corporate transactions are required to undergo independent valuation report like rights issues, material transactions and merger between publicly listed company and company. The OJK Regulation No. 35/POJK.04/2020 says that a valuator must be a licensed appraiser and registered by the Finance Ministry (MAPPI-certified or its equivalent). This level of regulation imparts a formal, compliance-oriented nature to business valuation Indonesia engagements, which must be comprehended by the professionals at the very beginning.

Besides compliance, it is valuations that motivate pragmatic decisions. With a logistics start-up in Bandung that has raised a Series B in 2023, the founders and investors spent a significant amount of time negotiating the independent valuation report, not because the methodology was not clear, but because both parties were not accustomed to working with a formal Indonesia business Valuation Report and did not fully understand how certain adjustments (working capital normalization, minority discounts) could affect the final number. It is one of the knowledge gaps that is common among junior finance practitioners and is the source of friction in real deal transactions.

How Three Core Valuation Methods Support Business Valuation Report Services Indonesia

Professional valuers of Indonesia have three primary methodologies on which they base their professional valuation and which are often used in the same assignment to overlap a band of values. The first thing in reading or writing a credible Indonesia business valuation report is to comprehend their logic and restrictions.

Table 1: Business Valuation Report Services Indonesia – Valuation Methodology Quick Reference

| Method | Core Logic | Best Used For | Key Limitation |

|---|---|---|---|

| Income Approach (DCF) | Present value of future cash flows, which are projected. | Companies that are profitable and have consistent forecasts. | Very sensitive to discount rate and forecasts. |

| Market Approach (CCA/PTM) | Comparison with similar listed transactions or companies. | Companies that are identifiable peers. | It is hard to find really similar Indonesian counterparts. |

| Asset Approach (NAV) | The difference between the fair value of net assets and liabilities. | Firms that are asset-heavy, holding companies, distressed cases. | Disregards the going-concern earning power. |

| Excess Earnings Method | Isolates the returns of tangible assets and the intangible earnings. | Companies that have a goodwill or brand value. | Needs in-depth analysis of intangibles. |

In the majority of Indonesia business valuation services engagements, the Discounted Cash Flow (DCF) methodology is the methodology of choice, with the Market Approach serving as a back-up. In the case of property-intensive businesses: plantation companies in Kalimantan or hotel chains in Bali, the Asset Approach is significantly more important. A properly formulated report will never fail to justify the reasons why a certain method was selected to be used in the first place, and the weighting adopted in case there was a reconciliation of more than one method.

Special attention should be paid to the discount rate in a DCF that is usually represented as the Weighted Average Cost of Capital (WACC). In Indonesia, a country risk premium should be added on top of the usual CAPM inputs by the practitioners. This premium has been between 2.5 and 4.5% as per the recent engagements based on the industry and the exposure of the company to the rupiah volatility. To the junior professionals reading a report, the most common method of determining the credibility or over-rosy nature of the valuation is to study the WACC build-up.

5 Major Steps in Business Valuation Report Services Indonesia Engagement Process

Any business valuation Indonesia engagement, regardless of whether you are in an advisory firm, a corporate finance team, or a client company preparing to transact, will generally occur through a systematic process. Knowledge of these steps will enable professionals in all levels involved to make a contribution and make the right questions at the right time.1. Scope and purpose definition – The engagement team and the client should agree prior to the data being gathered on the purpose of the valuation (investment, compliance, litigation, internal planning), the standard of value used (fair market value vs. investment value vs. liquidation value) and the valuation date.

- Scope and purpose definition — Before any data is collected, the engagement team and the client must align on the purpose of the valuation (investment, compliance, litigation, internal planning), the standard of value being applied (fair market value vs. investment value vs. liquidation value), and the valuation date. Making this mistake brings downstream issues.2. Data collection and due diligence – This is the most time consuming step.

- Data collection and due diligence — This is the most time-intensive phase. The team collates audited financials (at least three years), management accounts, legal documents, and contracts, asset schedules, and industry data. In the case of the Indonesian firms, this step usually brings up quality concerns, such as unaudited financials, related-party transactions, or informal revenue that makes the process of normalization difficult.3. Financial normalization and analysis – Raw financial statements are modified to reflect non-recurring items, owner compensation adjustments, and related-party price distortions.

- Financial normalization and analysis — Raw financial statements are adjusted for non-recurring items, owner compensation adjustments, and related-party pricing distortions. The result of this step is the normalized earnings base which is the driving force of the valuation model. In the case of family-owned businesses in Indonesia, this stage can be quite a delicate negotiation with the management on what is really operational as opposed to personal.4. Construction of models and application of methodology — The main and secondary models of valuation are constructed.

- Model construction and methodology application — The primary and secondary valuation models are built. To a DCF, this would entail building a five to ten year prognosis with a set of transparent assumptions, a calculation of the terminal value, and an estimation of the WACC. The model is then it is stress-tested on major assumptions to show how the value varies based on increase or decrease in revenue growth or margin.5. Report preparation, review, and sign-out – Final Indonesia business valuation report is prepared to professional standards (MAPPI, IVSC or as necessary by OJK).

- Report drafting, review, and sign-off — The final Indonesia business valuation report is prepared according to professional standards (MAPPI, IVSC, or as required by OJK). It contains an executive summary, the explanation of the methodology, the key assumptions, and sensitivity analysis, and the range of the concluded values. Reports to be used in either regulatory or litigation settings must not be signed off without senior review and quality control.

Understanding Valuation Reports in Business Valuation Report Services Indonesia: A Practical Framework

Critically reading an Indonesia business valuation report prepared by another junior finance professional is perhaps the most valuable skill that a junior finance professional can enhance. Reports may be 40 pages or more, and it is the knowledge of where to concentrate on that enables you to draw out the judgment calls of paramount importance that the valuers made. The four-step model below is a common Indonesian advisory firm training model.

Table 2: Business Valuation Report Services Indonesia – Four-Step Framework for Reading a Valuation Report

| Step | Focus Area | What to Look For | Red Flag if Missing |

|---|---|---|---|

| Step 1 | Anchor on Purpose | Read the engagement scope: What is the valuation date? What standard of value was used? | No stated purpose or valuation date — report may be misapplied |

| Step 2 | Examine the WACC | Check the discount rate build-up: Is the beta from a relevant Indonesian peer set? Is the country risk premium current? | Generic global WACC with no Indonesia-specific adjustments |

| Step 3 | Challenge the Forecast | Revenue and margin projections drive everything in DCF. Are growth rates supported by historical performance? | Projections significantly above historical averages with no explanation |

| Step 4 | Check Sensitivity Tables | Does value change reasonably if WACC moves ±1% or revenue growth drops 2%? Is a range presented? | Single-point value with no sensitivity analysis — treat with caution |

This four-step process does not turn an individual into a professional valuator, but it develops the systematic scepticism that is required to create value in negotiations on deals, board presentations or investment committee reviews. According to the reports of many mid-level practitioners in the field of Indonesian corporate finance, this type of analytical discipline to pose disciplined questions of valuation reports and not take numbers at face value is what makes the difference between a good and an excellent analyst.

Common Problems and Real Case Lessons in Business Valuation Report Services Indonesia

Actual interactions in Indonesia seldom proceed with complete smooth sailing and the difficulties are usually educative. Take an example of a manufacturing firm in East Java who has employed the services of a Jakarta-based advisory firm in a business valuation Indonesia exercise in advance of selling a minority stake to a Japanese strategic investor. The company was experiencing a high growth in revenues but inconsistent expenses reporting – part of personal expenses of the owner had been expensed through the business over the years. It replaced about IDR 4.2 billion of annual expenses with the normalization process, which significantly increased the normalized EBITDA and, consequently, the valuation ended. The Japanese investor team objected to all the adjustments made by the valuers in the due diligence exercise and the valuers had to furnish supporting documentation of every normalization item. The originally planned engagement of six weeks lasted almost four months.

Practical learning, and broadly applicable as well, is that in preparing a valuation engagement a company should be proactive in cleaning up its financial reporting at least one to two years before the time of the event. Normalized already well-documented financials cause much less friction and, in many cases, result in improved valuation results due to the time the valuers are in the business instead of re-creating its accounts.

Table 3: Business Valuation Report Services Indonesia – Common Challenges in Indonesian Valuation Engagements

| Challenge | Why It Occurs | Practical Response |

|---|---|---|

| Unaudited or not consistent financials. | Most SMEs are on informal accounting; family owners combine personal and business expenses. | Require at least 3 years of audited statements; require normalization adjustments to be documented explicitly. |

| Absence of similar Indonesian social friends. | Only a few companies in the sub-sectors listed on the IDX; the trading volumes are small and skew the multiples. | Use regional (ASEAN) peers having a size/liquidity discount adjustment. |

| Sensitivity to currency and inflation. | IDR volatility has an impact on WACC inputs and replacement costs on assets. | Make present value decisions in both IDR and USD; specify FX assumptions. |

| Regulatory compliance delays | OJK or MAPPI review will prolong report completion. | Establish regulatory review time in the timeline of engagement. |

| Disagreement on minority/control premiums | The stakeholders who are not usually acquainted with the notions of discount for lack of control (DLOC) concepts. | Train customers on discount reasoning as early as possible; provide simple language explanation in the report. |

The other typical trend in Indonesia business valuation services engagements is the market approach. As part of a 2024 deal in the Indonesian healthcare industry, the valuers chose an Indonesian, Malaysian and Thai set of five publicly listed hospital groups as the comparable company set. A single Indonesian peer was eventually locked out of the final analysis due to being delisted and its most recent trading price indicated that it was in distress and not a reflection of its underlying value. It is a type of judgment call whereby the experience of the lead valuator is important, the types of comparables to include, how to use the appropriate size or liquidity discount, and where junior professionals must listen in on during review meetings.

Table 4: Business Valuation Report Services Indonesia – Typical Valuation Engagement Timeline

| Phase | Typical Duration | Key Output |

|---|---|---|

| Scoping & engagement setup | 1–2 weeks | Engagement letter, data request list |

| Data collection & due diligence | 2–4 weeks | Normalized financial model, industry analysis |

| Model build & methodology application | 2–3 weeks | Draft valuation models (DCF, comparables) |

| Report drafting & internal review | 1–2 weeks | Draft report for client review |

| Client review & finalization | 1–3 weeks | Final signed report |

| Regulatory submission (if required) | 2–6 weeks (variable) | OJK-approved / MAPPI-certified report |

Building a Career in Business Valuation Report Services Indonesia

The career options of professionals interested in a career in Indonesia business valuation services are clear-cut and however, need a conscious investment in their technical expertise and qualifications. The Masyarakat Profesi Penilai Indonesia (MAPPI) qualification is the best known national qualification of the appraiser whether in real property valuation or business valuation. The Chartered Financial Analyst (CFA) designation and the Business Valuation credential of the American Society of Appraisers (ASA-BV), are recognized internationally in the context of cross-border transactions.

In addition to credentials, the best method of acquiring expertise is by being subjected to organized exposure to live engagements in various industries. The former will create a more informed perception of how industry dynamics influence financial forecasts and similar selections than will someone with many years of experience in one industry. The Big Four accounting firms, advisory firms and the valuation departments of the large Indonesian banks are all good places to start.

Another aspect worth mentioning is that the need to have credible business valuation Indonesia work is being propelled more by the maturing startup ecosystem in Indonesia. As the number of Indonesian technology and consumer companies look for Series C and subsequent-stage funding, or even an eventual IPO listing on the IDX, their founders and boards need valuation advisors who are both savvy of the technical requirements and the business expectations of external investors. This generates an authentic high value among those professionals who can narrow that divide – to convert rigorous local methodology to internationally readable conclusions.

Conclusion: Key Takeaways and Next Steps

Professional Indonesia Business Valuation Services are at the crossroads of financial rigor, regulation and business judgment. When it comes to junior and mid-level professionals, there is no hidden secret on how to become competent. It involves the methodological knowledge that is systematic, familiarity with the actual processes of engagement that is repeated and the ability to read reports critically instead of passively.

The growth trend of the Indonesian market, coupled with the growing OJK control and a growing number of foreign investors willing to have credible documentation of Indonesia business valuation report, implies that the number of practitioners will be in demand. Whether it is your first engagement, or you are seeking to enlarge upon the practice you already have, the principles discussed in this article form a sure base.