Certified Business Valuation and Accounting Training

Impact of Financial Statements on Business Valuation

Guide on Certified Business Valuation and Accounting Training

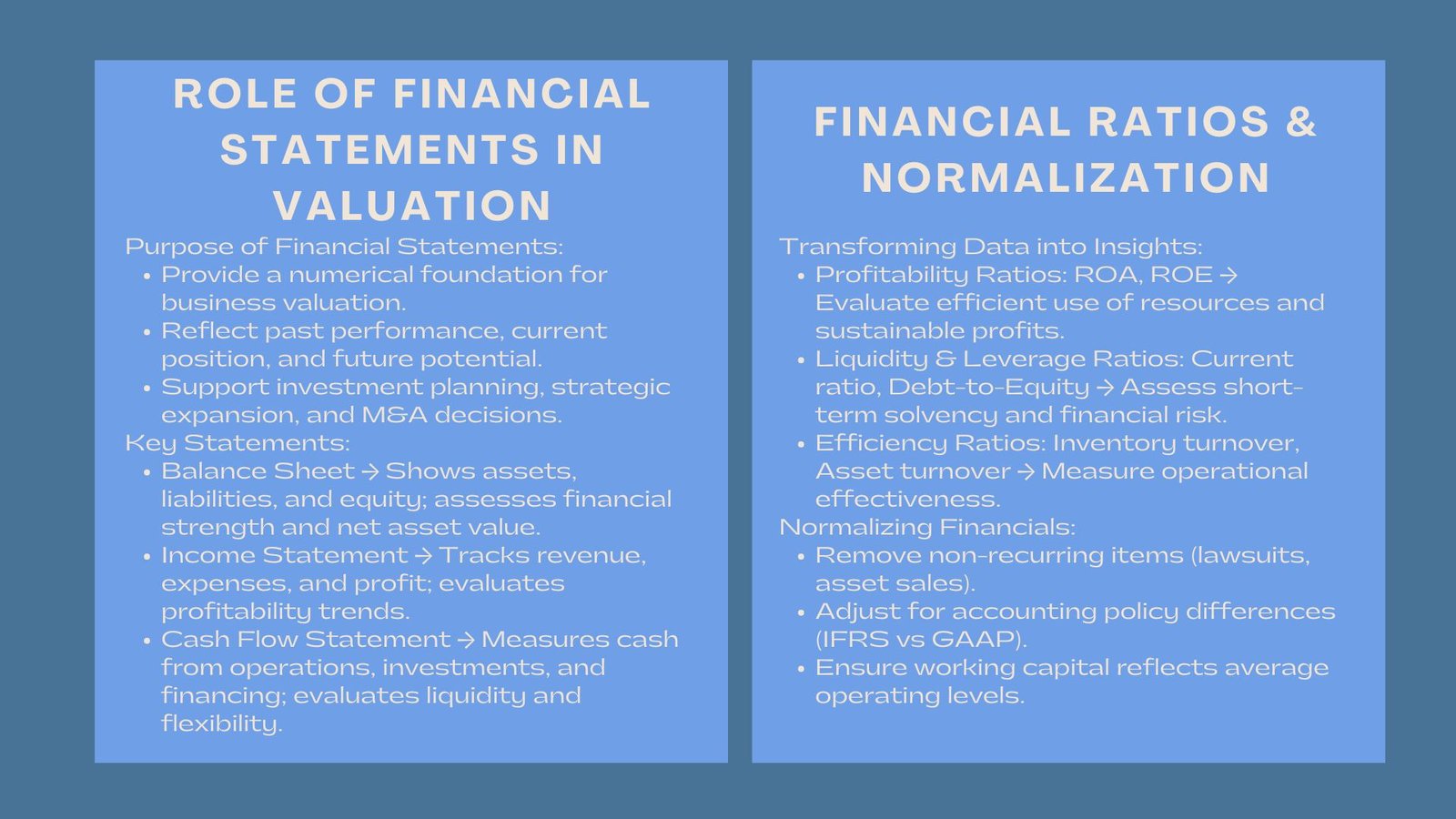

Any credible business valuation is based on financial statements. They contain the pure numerical support reflecting the previous performance of a company, its current status, and future opportunities. In the absence of proper financial information, the investors, analysts or acquirers would hardly know the true value of a company.

It takes a lot more than a simple look at profitability to do an in-depth valuation of an enterprise, it takes a profound comprehension of the manner in which assets, liabilities, revenues and expenses are interconnected to create value of an enterprise. Financial statements provide that level of clarity; that is, business actions into measurable information that assists in forming decisions, investment planning, and strategic expansion.

The Fundamental Use of Financial Statements in Valuation.

Business valuation is intended to establish the reasonable economic worth of an organization. To do so, the financial statements serve as the basis, on which the valuation models and assumptions are based. They allow analysts to determine the earning capacity, liquidity, solvency and the efficiency of the capital of a firm.

Historical Financial Data as the Point of Departure.

The starting point of valuation is the analyzers examining the past history of a company; the past three to five years. Revenue growth trends, profit margin trends, and operating efficiency trends indicate whether a business is experiencing a sustainable growth in profits or it is under financial pressure. Precise information on the past can also be used to make realistic predictions about the future performance.

Forecasting Future Value

Valuation depends on the projections of the future. Historical financial statements help the analysts to formulate the future cash flow, capital expenditures and working capital needs. The projections are then discounted in present value on the basis of the cost of capital in the company. A decent forecasting model could be achieved only when the historical financial statements are true and comparable.

Important Financial Statements to Motor Business Valuation.

Every financial statement narrates different aspects of a company. Analyzed in combination, they give the 360 view of financial health and performance potential.

The Balance Sheet – An Evaluation of Financial Strength.

The balance sheet is a statement that shows the assets, liabilities and equity of a given company at a particular period of time. In terms of valuation, it assists in the determination of net asset value and evaluation of financial stability. Good industry balance sheets and low leverage are positive indicators that tend to improve valuation, and too much liabilities will reduce investor confidence.

When valued in the right manner, assets like property, plant and equipment form a physical support of the value of a firm in the market. In the meantime, intangible assets such as patents or goodwill can be of great importance in knowledge-based industries.

The Income Statement – Profitability Measuring.

Income statement gives an insight on the efficiency of a business to make profits out of the business. It captures revenues, expenses, and net income at a time, which enables analysts to evaluate the trend of profitability and operational performance.

This statement is converted into ratios including gross margin, EBITDA margin and net profit margin among others, which are used to compare the performance of a company with others in the same industry. The high valuation multiple is normally connected to a consistent profitability.

The Cash Flow Statement – An Introduction to Liquidity.

Here, as well as performance, liquidity is a performance of financial flexibility. Cash flow statement follows the flow of cash within a business whether it is an operating, investing or a financing activity.

A positive operating cash flow represents great business fundamentals and helps in giving greater confidence in valuation. Conversely, firms that are always dependent on external funding to finance their deficit can get a low valuation.

Financial Ratios: Converting Data into Valuation Data.

Financial ratios are used to convert raw statements data to actionable measures of valuation. These ratios are used by analysts to rank companies and determine their strengths and weaknesses which affect valuation performance.

Profitability Ratios

These indicators like Return on Assets (ROA) and Return on Equity (ROE), show how well an organisation utilizes its resources to achieve profit. The high and steady ROE businesses are normally valued highly due to the fact that they are an indicator of high management performance and capital efficiency.

Liquidity and Leverage Ratios.

The liquidity ratios such as current ratio indicate the capability of a company to fulfill its short-term liabilities, whereas the leverage ratios such as debt-to- equity ratio reveal the risk of capital. Over leverage can cause a decrease in valuation because of increased risk of default, and balanced leverage can maximize capital efficiency.

Efficiency Ratios

Efficiency ratios include inventory turnover, asset turnover, etc; they show the efficiency or inefficiency of the company regarding its assets to generate revenue. High efficiency does mean that there is improved operational management, and tends to result in increased perceived value.

In professional analysis, firms often rely on comprehensive financial statement review and valuation modeling services for business acquisition and investment decisions to ensure ratio interpretations are accurate and consistent across reporting periods.

Rebates and Re-pricing in Financial Valuation.

Not every reported financial performance illustrates the actual economic performance of any company. To eliminate any unusual or one-time activities that can lead to distorted values, analysts tend to make normalizations.

Elimination of Non-Recurrent Items.

The settlement of lawsuits, costs to restructure or a one time disposal of an asset have been excluded to paint an earnings picture that is normalized. This will enable a better prediction of future sustainable incomes.

Hedging against Accounting Policy Differences.

The financial outcomes may vary due to various accounting rules (e.g., IFRS vs GAAP) or depreciation means. These differences are adjusted by the valuation analysts in order to make comparisons between companies and industries.

Normalizing Current Assets.

The working capital change may have much influence in the calculation of free cash flow. Adoptions are made to guarantee that the figures reported are the average operating levels and not temporary.

Connection of Financial Statements and Valuation Models.

Discounted Cash Flow (DCF), Comparable Company Analysis and Asset-Based Valuation valuation methods are very reliant on financial statements.

Discounted Cash Flow (DCF) Method.

DCF method predicts the free cash flows in the future based on income statements and cash flow statements. These estimates are discounted to present value through a discount rate that is dependent on the balance sheet capital structure.

Market Multiples Approach

According to this method, the multiples of valuation such as the EV/EBITDA or P/E are computed with the numbers in the income statement. Quality financial statements will make comparison with other companies in the industry correct and relevant.

Asset-Based Approach

The approach utilizes balance sheet information to determine the worth of the net assets of a firm. Tangible and intangible assets have to be brought to realistic valuations as the fair value of the assets should be changed according to the present market conditions.

Businesses seeking accurate valuations often engage professional financial reporting and business valuation advisory services for corporate finance and transaction support to align accounting data with market-based valuation principles.

Ordinary Problems with the use of financial statements in valuating.

Although financial statements are very important, they do not lack limitations.

- The lack of consistency in reporting standards may complicate the comparison of jurisdictions.

- Ineffective disclosures can have the effect of concealing important information, e.g. contingent liabilities or off-balance-sheet financing.

- When transforming foreign financial statements into one currency, inflation and exchange rate variations may lead to distorting of the values.

The solutions to these problems are to make sure that the companies have transparent, audited and current reporting in accordance with international accounting standards.

Conclusion

Financial statements are not only historical documents but they are the basis of business valuation. Coupled with a balance sheet, income statement, and cash flow statement, one can have a comprehensive perspective of financial health and potential performance.

To analysts, investors and acquirers, the knowledge of the relationship between the financial statements and valuation models means that they make a more proper judgment of the true worth of the company. Quality financial reporting does not only enhance confidence in the market, but also aids in informed decision-making in mergers, investments and long term strategy.