Why Is Company Valuation Important?

A practical guide for junior to mid-level finance and business professionals

Introduction to Why Is Company Valuation Important?

The valuation of companies is the estimation of a company’s worth at a specific time. It’s important because almost all major business decisions, including capital raising, equity sales, competitor acquisition, employee compensation, or succession planning, require a believable, well-documented business opinion of value. If it’s not in place, businesses are negotiating in the dark, investors are unnecessarily taking risks, and regulators are not provided with evidence to evaluate compliance. Knowing the importance of business valuation and how it functions is actually a crucial skill for any finance and strategy practitioner.

Key Takeaways

| ✦ | Business valuation is required throughout the entire life of a business, from start-up to exit or succession. |

| ✦ | In the process of valuation, a common language is created between founders, investors, acquirers, and regulators, with information asymmetry reduced in the negotiations. |

| ✦ | The valuation isn’t a single event, but rather a collection of steps that use various methods to assign a value to a business, and there is no one ‘right’ way to value a business, as different methods are appropriate for different purposes, and the same business can have multiple defensible values at the same time. |

| ✦ | Knowing why companies need valuations can aid professionals to expect when the valuation exercise will be required to be set in motion and what the inputs will be. |

| ✦ | Typical errors include inappropriate comparison of values for the context, financial data that is normalised too much, and choosing non-comparable peers. |

What Does Company Valuation Actually Mean — and Why Does It Come Up So Often?

In essence, a business valuation is a well-informed estimation of business value. It is not an exact measurement, but a well-informed and organized view which is based on financial information, market evidence, and analytical judgment. A business valuation is often requested during significant milestones throughout a company’s journey — whether it is raising a round, considering a sale, adding partners, restructuring equity, or simply wanting to gain a better understanding of how their company is doing versus the competition.

The key to the importance and complexity of valuation is that it is value dependent. A strategic acquirer’s valuation is based on the value he or she thinks he or she will be able to realize the synergies of the acquisition, which could be quite distinct from what a financial investor would seek to pay for the same business. In the same way, the value used for a regulatory filing (such as for estate and inheritance tax) would differ from the value agreed in a private transaction. People aware of these differences are much better equipped to be effective in making high-consequence decisions.

One crucial fact that many junior professionals can learn is that valuation talks occur all the time, not just when it comes to formal deals. There is a valuation assumption within every board meeting when they are thinking about the acquisition; there is a valuation assumption in every CFO’s mind when he or she is thinking about a share-buyback; there is a valuation assumption in every founding team’s mind when they are considering giving equity to a new hire. The ability to assimilate the logic of value creation is thus a skill, and a strategic one.

Why Do Companies Need Valuation at Different Stages of Their Growth?

There’s no one right way to do business valuation. A seed startup looking to its first institutional round has a very different valuation problem than an industrialized business that is looking to sell its business in a management buyout. But in both instances the same basic question comes up: What is this business worth—and why?

In its early stages, valuations are frequently more about the story than the numbers. The company’s revenues can be quite small, profits may be scarce, and the business model is likely still being established. At this point, investors are trading on a team, a market opportunity, and a hypothesis. The valuation is a critical component that sets expectations on terms and rounds and is the limit of what equity shareholders will sell for capital. It is a mistake to do either, as the subsequent round of funding could be a down round, and the founders could have given up too much too soon.

The principles underlying the value of a business evolve as the business grows. There will be greater predictability of revenue, margins will be more stable, and there will be a history of financial performance to review. At this point, market-based techniques (such as a comparison of similar companies and analysis of precedent transactions) are more significant as there is enough data available to make meaningful comparisons. In a strategic sale, or when a company is going out on an IPO, it is common for a company to hire a firm to do a formal valuation to test their own assumptions, to prepare for their board’s presentation on the valuation, and to account for the questions that institutional investors (or acquirers) might ask. That’s why companies need to be valued at more than just transactional moments — it’s a way to be financially prepared.

What Are the Five Core Situations Where Valuation Becomes Unavoidable?

Here are five time periods when it makes sense – and is necessary – to hire a business valuation service. They have unique expectations regarding methodology, rigor, and audience.

As for an equity transaction (private equity, venture capital, or strategic investor), there has to be a common understanding regarding the pre-money valuation. The valuation is used to determine the amount of the business that will be sold for the funds raised and to set the expectations of the performance going forward.

In the case of M&A, the value is the basis for the entire deal. These are the things that buyers want to know, and sellers want to know about them. A savvy seller will start a process with a valuation analysis all their own, even though not to set the price, but to communicate its value believably in the minds of buyers.

Employee Equity and Incentive Plans: Stock option grants, restricted stock units, and other equity-linked incentive plans all demand a defensible value of the underlying stock. This is not only a best practice in many jurisdictions, but a regulatory requirement as well. If the strike price is set too low, the tax liability may become an issue; if it is set too high, no one would be motivated to take advantage of the strike price.

Regulatory, tax and legal purposes: Formal, documented valuations are needed for cross-border transactions, estate and gift tax filings, shareholder disputes and bankruptcy proceedings and will withstand challenges from tax authorities, court and regulators. The value of these situations and the amount of rigour required is usually more stringent than in a private negotiation.

Outside of transactions, periodic valuation allows management teams and boards to determine whether they are creating or destroying value over time, how they measure up to other companies, and where they should turn to for capital to get the best return. This is the most obscure, but possibly one of the most useful valuations that can be used internally.

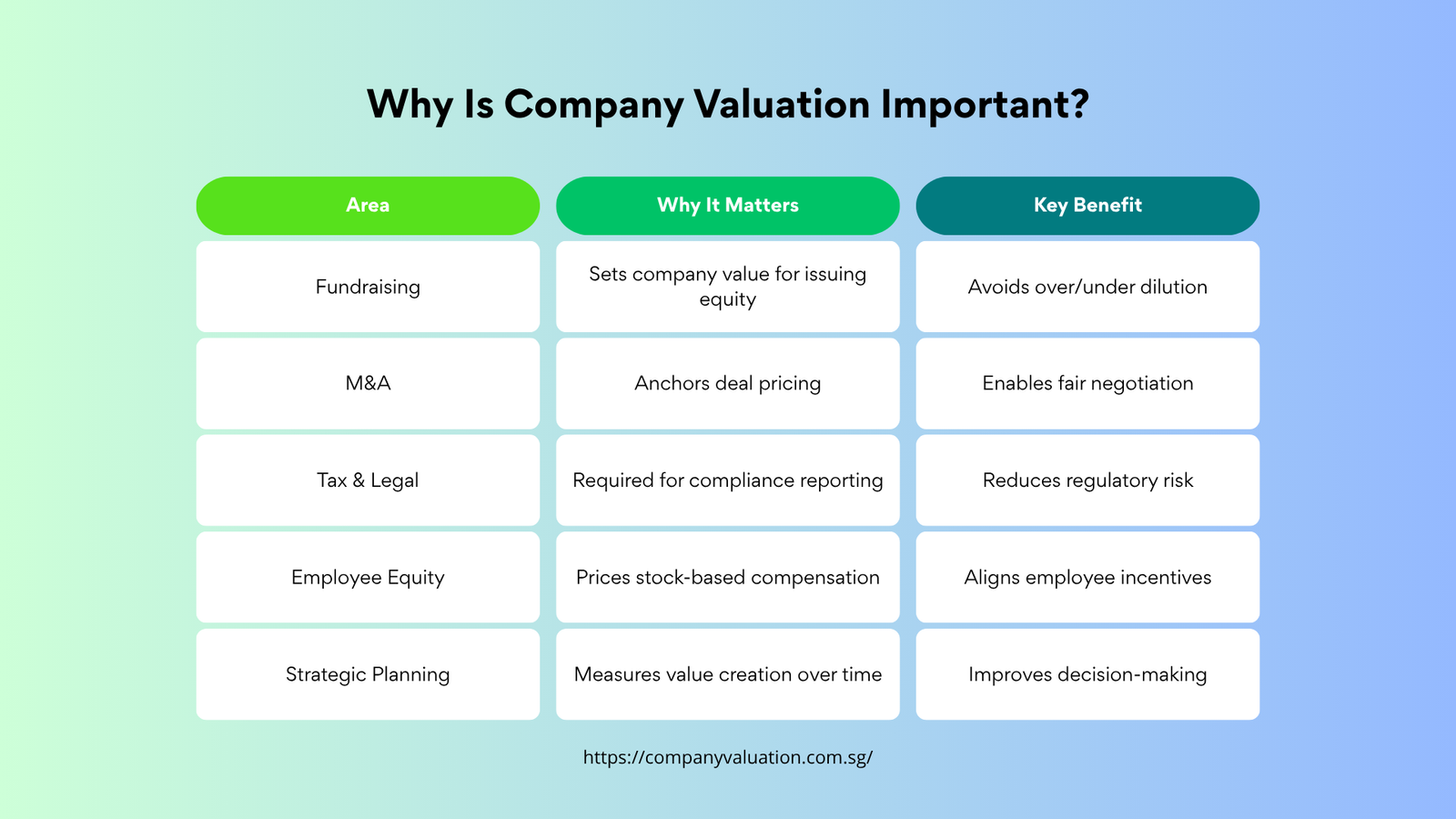

Table1: When Valuation Becomes Essential: A Situational Overview

| Situation | Why Valuation Matters | Common Stakeholders |

|---|---|---|

| Fundraising & Investment | Determines equity dilution and sets the price that equity is issued at. | Founders, VCs, Angel investors |

| M&A Transactions | Sets a reasonable price for customers and vendors; assists in negotiating | CFOs, Boards, M&A advisors |

| Regulatory & Tax Compliance | Welcomes transfer pricing, estate planning, and statutory filings. | Tax teams, Legal counsel |

| Employee Equity Plans | Calculates the exercise price of an option on a share (such as a 409A in the USA) | HR, Finance, Employees |

| Strategic Planning | Compares performance to peer groups and guides capital investments. | CEOs, Strategy teams, Boards |

How Do Real Cases Illustrate the Consequences of Getting Valuation?

WeWork’s share of the attempted 2019 IPO will serve as one of the most informative valuation case studies of the last 10 years. The company was valued at $47 billion at its height, largely by the lead investor for the company, who was interested in the company not as a technology firm but as a disruptor of the commercial real estate sector. Once the investors in the public markets did a business analysis and looked at the actual numbers, they were soon presented with a venture that was essentially a property company with a tech coat on, and a business that was well on its way to losing money. The IPO was cancelled, the valuation plummeted, and the incident changed the investors’ mindset about growth-stage companies that straddle sectors. The lesson learnt was not that valuation is not relevant to pre-profit companies, but rather that valuation narratives need to be grounded in sound financial logic, rather than simply vision.

The better positive example is, of course, the LinkedIn acquisition by Microsoft in 2016, which was valued at about 50 percent over LinkedIn’s trading price at the time of the acquisition. That high price seemed like a lot of money on the books. However, Microsoft’s in-house valuation exercise was more about LinkedIn as a data and productivity component that can be used throughout its enterprise software portfolio. The pricing of the deal was based on the investment value — of LinkedIn particularly to Microsoft — not fair market value. That’s the key to the need for business valuation in an M&A: It’s not what is the value of this business, but what is the value of this business in this context, with these synergies?

A third example is Facebook’s 2012 purchase of Instagram for $1 billion dollars for a company with just thirteen employees and no revenue — which was ridiculed at the time as an insane amount of money being spent on a business with no income. The transaction on any of the traditional valuative criteria seemed futile. But Facebook’s thinking was based on a strategy that mainstream valuations were not given credit for: what it’s worth to remove the competition for a long-term market they can’t capture, and what it’s worth to acquire a fast-growing user base of engaged users. Ten years later, Instagram was making tens of billions of dollars in revenue each year from advertising. It’s important to note that the requirement to use business valuation frameworks with flexibility to account for business optionality and network value is not that fundamentals are not important; it’s just that it’s important.

What Does a Rigorous Valuation Process Look Like in Practice?

It’s important to grasp the importance of business valuation, but knowing how a quality valuation process is actually run is what makes professionals truly useful in the room. A thorough valuation process has a standard structure, but the steps to be taken will depend on the purpose and the size of the business.

Table 2: The Six-Phase Valuation Process

| Phase | Key Activities | Output |

|---|---|---|

| 1. Define the Purpose | Discuss the reason for the valuation and the adopted standard of value (fair market value, investment value, or other). | Engagement brief or mandate letter |

| 2. Gather Information | Collect financial statements, management accounts, contracts, customer information, and market intelligence. | Normalised data set |

| 3. Industry & Market Analysis | Discuss growth and competition in the sector and macro indicators which impact the business. | Market context report |

| 4. Apply Valuation Methods | Introduce income-based and market and asset-based processes; create sensitivity analysis; | Preliminary valuation range |

| 5. Reconcile & Conclude | Adopt the methods based on risk profile within the organization; adapt to suit | Concluded value opinion |

| 6. Report & Communicate | Create methodology and assumptions documentation and findings for intended audience | Valuation report or board memo |

The initial step – defining the purpose – is often underestimated. The standard of value (whether it’s the ‘fair market value,’ ‘fair value,’ ‘investment value’ or any other value standard) dictates the decisions that follow with respect to methodology, peer selection, and adjustments. People who neglect this step tend to create technically sound work that does not apply to the purpose.

Financial data is equally important to normalise in phase two, and is sometimes more time-consuming than it sounds. One-time expenses, financial results related to private company owner compensation that are outside of market rates, arms-length transactions that never existed, etc. often are included in the financials of private companies. If they don’t adjust for these items, then they’re creating a false impression of underlying profitability, and that translates into a false impression of valuation. The difficulty is multiplied when companies have operations in other jurisdictions that may have different accounting principles, or management accounts vary significantly from the audited accounts.

The most frequent error made by young professionals is to view the settled value as an actual value, not a range of values. A good valuation practice is to include an “expected” value as well as a sensitivity analysis that includes the changes in value if different growth, margin, or multiple assumptions are made. This lends credibility to the sophisticated audience because they have heard that things may not be as they are now, and that this is an admission.

Why Is Company Valuation Important: Frequently Asked Questions

When is it a good idea for a company to have a formal valuation?

There is no one right answer, but most advisors feel it’s best to have a formal exercise when a major event is coming up, such as a funding round, a potential sale, a regulatory filing, or an equity incentive plan is about to be executed. One is commissioned every year by many private companies at maturity stage, as part of best governance practice.

Does the value of a company vary with the questioner?

Yes, and this is one of the most vital in the field. A strategic buyer (who considers synergies) can value the same business differently than a financial buyer (who values it based on cash flow returns), which in turn will be different than the tax authority (who values it based on a statutory standard). Knowing this is a key aspect of the importance of business valuation literacy.

Price vs Value?

Price is the actual amount that a buyer pays in an exchange; value is an analyst’s estimate of the worth of something by evidence and methodology. These two are frequently not the same, particularly depending on negotiating dynamics, the prevailing market mood, and information each party has available.

What is the point of having a company valued if it’s not being sold?

Since business is all about creating value. Without the need to go through an actual transaction, regular valuation benchmarks enable management to determine if strategic decisions are effective, guide capital allocation decisions, and determine the equity-based compensation for employees.

Conclusion: Actionable Insights for Professionals

Business valuation is not just a technical exercise confined to any particular niche — it’s a thread that is woven through every important business decision. Whether you’re just starting to talk about raising money, or you’re getting ready to exit, whether you’re selling to your employees or filing applications with regulators, a good, well-thought-out idea of value is what sets companies apart that do it well, from those that do it poorly.

If you’re a junior or mid-level staffer looking to advance your career in finance, strategy, or corporate development, three practical steps will help propel your progress in this area. First, learn about genuine transactions. In every announced deal or IPO, there is embedded valuation logic – a multiple implied by the deal price, a premium over trading value, and a strategic rationale, which is the logic behind paying above market. Read through the press releases, the analysts’ commentaries, and (where applicable) investors’ presentations; learn to work backwards. Second, familiarize yourself with all of the techniques. Many people opt for what they are used to or what is the simplest for them. True competency lies in being able to trust market multiples, use a DCF to support your analysis, and pick the right asset-based approach. Third, ask the question: always, WHY are companies valuing in this particular circumstance? WHY determines the method, the method determines the output, and the output determines the decision.

The essence of valuation is better decision-making in the presence of imperfect information. It’s the professionals who master it who aren’t the ones who get the ‘right answer’ — they’re the ones who ask the right questions, put together the most solid logic, and clearly and forcefully communicate it.